Thursday, January 31, 2013

Mewah

Mewah: industry sources say Msia’s biggest palm oil refiner after Wilmar, will revive an earlier plan to build a palm oil refinery in east Malaysia, after the govt's decision to reform its export taxes.

The govt has said it will scrap a duty-free quota on CPO exports and at the same time reduce export duty on CPO, which will boost the Malaysian refining industry's competitiveness in processing palm oil products.

The lower duty should keep domestic CPO prices low, and help to encourage domestic refining.

The construction of the palm refining plant, which will have an annual capacity of 0.5m tons, is scheduled to be completed in 3Q13. Mewah currently has an annual refining capacity of 2.8m tons in Malaysia.

Mewah had delayed construction of the Malaysian refinery early last year so that it could focus on building one in Indonesia instead. Indonesia had changed its palm oil tax structure in Oct 2011, allowing its refiners access to cheaper feedstock, and helping Indonesian processors to boost margins to trump the established downstream palm oil refining industry in Malaysia.

Mewah’s strategic shift may allude to mgt’s confidence in better prospects going forward.

Mewah trades at 15.3x P/E, 1.2x P/B.

Iskandar/ Rowsley

Iskandar: continues to receive growing interest. JPM led a group of 25 investors from SG and KL for a tour of Iskandar, Johor property sites last wk, along with presentations by Iskandar Invmt Bhd (Khazanah -owned) , as well as Johor property stocks (ie. UEM Land, Sunway, WCT). JPM observes, the marketing trip points to strong, rising interest in Msia property plays (ex-REITs) given the segment's steep underperformance despite decent underlying on the ground fundamental , in lieu of the election overhang risk.

JPM reiterates its preferred plays for the Iskandar theme via smaller players.

In Spore, Rowsley is one of the few stocks with potential Iskandar exposure, through its proposed takeover of a Msian architect firm and Iskandar land acquisition via an issue of up to $581m in new shares (at issue price of $0.15/sh). Recall, the devt is slated for a $3b integrated mixed-use township comprising apts, malls, convention centres, yielding more than 10m sf of GFA.

The stock remains a concept play, with no earnings to speak of, and trading at 6.9x P/B.

Ezra

Ezra: DMG Insti Sales has a note out on Ezra, reiterating their BEARISH view on the stock. House rehighlight their recent post that Ezra's recent results illustrated problems in the sector with both rising costs and falling margins and that the street was being far too optimistic. Last night, Saipem, one of the world’s largest integrated oil and gas service providers, fell 34% yesterday after releasing their latest FY12-13 earnings guidance which were significantly lower than consensus by 50% (for FY13).

Saipem guided for 50% decline in FY13 EBIT overall but more importantly (from an EZRA viewpoint) they also said that they expected a 70-80% decline in onshore and offshore engineering and construction EBIT due to completion of high-margin projects, execution of lower margin contracts in FY13, delay in contract awards and investment in Brazil. Whilst the Brazil part doesn’t apply to EZRA, the rest clearly does

The reasons given by Saipem are consistent with house neutral/negative view on the offshore construction sector.

Think high wages, geographical expansion and competitive bidding will put pressure on operating margins for offshore construction players like Ezra Holdings and Swiber Holdings. Saipem released their revised earnings guidance for FY12 and FY13, whereby management expect FY12 EBIT to be lower 6% from their previous guidance and FY13 EBIT to fall 50% y-o-y. This new guidance simply highlights the ongoing margin pressure from the competitive environment. The latest guidance from the global giant in onshore and offshore construction supports our view that cost pressure and competitive bidding will put pressure on margins. Technically, Ezra has come off from the spike ahead of earnings post several downgrades and looks set to test the 50dma. Use a stop of any break above the $1.23 resistance line. EZRA looks very capped at $1.23.

Guocoleisure

Guocoleisure: is up 2% at $0.735 on above avg volume, extending yday’s price surge.

Co announced its 1HFYJun13 results last Friday evening.

Revenue at US$203.9m, +7.5% yoy, mainly due to higher revenue generated from the hotel segment during the 2012 Summer Olympics, which helped offset some weakness on the gaming side.

Net profit however fell 4.1% yoy to US$35.5m, as oil & gas income decreased 18% yoy due to lower avg crude oil px, and lack of a one-off royalty distribution of US$5.4m arising from settlement of a royalty dispute in the previous yr.

On outlook, mgt noted that the adverse situation in the Eurozone and UK continues to have an impact on the group’s hospitality business which is its largest segment. However, mgt expects contribution from the Bass Strait oil and gas royalty in Australia to remain strong. The group will also continue to focus on the disposal of its remaining assets in Fiji. Overall, mgt expects the group to perform satisfactorily.

The counter trades at 11.1x annualized 1HFY13 P/E, 0.68x P/B. Market watchers have tipped Guocoleisure as an undervalued asset play, particularly as the bulk of its assets comprise invmt properties and properties under devt.

In 4Q12, The Edge tipped that the retirement of Jeremy Hosking, a key founder-director of Marathon Asset Mgt, could be a prelude to privatization of the companies it has invested in – Guocoleisure being amongst the list. Hosking was known for value investing, and as an activist shareholder, resisted several buyout offers by major shareholders previously.

Rotary

Rotary: to lift trading halt at 2.30pm.

Secures an EPC contract worth ~$300m from Tankstore, for the expansion of the oil terminal at Pulau Busing, Singapore. The contract is for a period of two yrs and is expected to start immediately. The scope of work involves the engineering design, procurement and construction of a 800k cbm facility.

With this win, Rotary's current order book stands at ~$750m. This compares with FY11 revenue of $531m.

The co trades at 1.5x P/B, was loss making on a trailing 12m basis.

Ezra/ Swiber

Ezra/ Swiber: Ezra is down 0.8%, whilst Swiber is down 1.4% today. Saipem, one of the world’s largest integrated oil and gas service providers, fell 34% yesterday after releasing their latest FY12-13 earnings guidance which were significantly lower than consensus by 50% (for FY13).

Saipem guided for 50% decline in FY13 EBIT overall but more importantly (from an EZRA viewpoint) they also said that they expected a 70-80% decline in onshore and offshore engineering and construction EBIT due to completion of high-margin projects, execution of lower margin contracts in FY13, delay in contract awards and investment in Brazil. This new guidance simply highlights the ongoing margin pressure from the competitive environment.

OSK DMG noted that Street seems to be far too optimistic despite both the rising costs and falling margins on the sector. House think high wages, geographical expansion and competitive bidding will put pressure on operating margins for offshore construction players like Ezra Holdings and Swiber Holdings.

Yangzijiang

Yangzijiang: Counter down below the $1.00 mark declining 1.0% today. 3 days after the Company announced that Seaspan has exercised its option to purchase 4 additional unit of 10,000 TEU containerships with the Group, the Company announced on 27 Jan that they have put up 3 abandoned 2,500 TEU containerships for resale.

The three vessels were originally ordered by a German owner, with one of the three vessels already completed and the other two to be completed by May. Despite the owner having paid 40% down on the contracts, it has decided to cancel the contract due to sharply lower newbuilding prices. Currently Yangzijiang is looking for new buyers for the three vessels. According to vesselsvalue.com, the price for a 2,500teu containership which is schedule to be completed in 2013 is around US$23.3m.

We think the three vessels were originally ordered in 2007; values of such vessels were around US$50m then, but have fallen to about US$24m currently. Two of the five installments for each vessel have been paid up, accounting for 40% of the total contract value. With the 40% deposit, and assuming YZJ is able to sell the vessels at current prices, the difference per vessel is not substantial (~US$6m).

MLT

MLT: UBS reiterates Buy, raises TP to $1.24 from $1.13. Notes over the past two yrs, MLT has consistently acquired assets to grow its earnings base, a trend the house believes will continue. With a $1b pipeline in various stages of completion, UBS thinks the sponsor will provide an impt growth platform for MLT, particularly as organic growth is slowing. Raises FY14-16e earnings by 2-4% and its 5-10 yrs growth trajectory by 1ppt to 2.5% inline with the growth mkts that MLT is targeting.

CDL Hospitality Trust

CDL Hospitality Trust: OSK DMG released a report on Company, that uncertainty in the market remains. House noted that although the market has somewhat stabilized in 4Q12 on the back of a relatively strong festive season, with a weaker calendar year of events in 2013, particularly during 1Q13, they believe the earnings of the Company will be under pressure as competition in the hospitality sector continues to grow. Competition is also expected to be strongest in 1Q13 as 36.2% of 2013 total supply of hotel rooms are expected to come through during this quarter.

Given a tight supply in the labor market of Singapore, management indicated that more initiatives would be introduced in the coming months to cut down on the hotels’ dependence on labor. In addition, a system which allows the Group to share pools of labor within its group of hotels will also be introduced in the coming months.

OSK DMG maintain NEUTRAL with unchanged TP of $2.05 on CDL Hospitality Trust.

IndoAgri

IndoAgri: UBS believes the acquisition of CMAA (a sugar grower and processor) in Brazil could add 5% to net profit in 2014 and rise further to 16% in 2016. NAV of US$77m translates to 5% of the current share price. Says, on an EV/ton and EV/EBITDA basis, the acq looks fairly priced, but it is worth noting that CMAA has lower cash costs and higher sugar contraction than the industry.

Notes IndoAgri still has US$100m in cash at the co level, and continues to look for potential expansion opportuniteis (whether organic or through acquisitions) and plans to continue to look for invmts in palm oil, sugar and rubber.

UBS keeps its Buy rating with TP $1.57. Adds, the co trades at 8.8x FY13e P/E, cheaper than Golden Agri's 10.8x and the sector's 11.6x.

Elektromotive

Elektromotive: proposes 10-into-1 share consolidation, subject to approval by SGX and sh/h at an EGM.

Transcu

Transcu: is acquiring 74.8% stake in Nanomizer for $41.0m from Forest Pine Group. With the acquisition, the group is set to benefit from the commercialization of the Nano-Emulsion Fuel System and return to profitability over time. It will issue 3,155.8m new shares at $0.013 per share (at prevailing market price) to Forest Pine Group. Nanomizer is valued at no less than US$112.8m by an independent valuer and Transcu's 74.8% stake in the share capital amounts to US$84.4m. Transcu's current market cap is $46m.

Transcu is acquiring the business at a 60.1% discount to

current valuation.

Halcyon Agri Corporation Ltd (IPO)

IPO tomorrow would be for Halcyon Agri Corporation Ltd. A midstream natural rubber producer, specialising in the production and marketing of natural rubber for the global tyre manufacturing industry. The Company is headquartered in Singapore and owns several rubber processing facilities in Indonesia.

Placement details of 61m shares at $0.36 each as follows:

44m new shares;

17m vendor shares;

Company is pricing IPO at 16x P/E, vs peer GMG Global at 18.8x P/E

Genting SP

Genting SP / LVS results: UOB Kay Hian has a read through in LVS results. House note that MBS’ RCV jumped impressively, but GGR and EBITDA remain depressed. LVS 4Q12 report card revealed that MBS rolling chip volume (RCV) rebounded sharply in 4Q12, recording a growth of 45% yoy and 37% qoq to S$20.1b. However, VIP GGR recorded a 7% yoy contraction to $430.9m as the RCV win was lower at 2.14% (4Q11: 3.34%, 3Q12: 1.79%). Meanwhile its non-rolling chip vol continued to languish both on a yoy and qoq basis by 3.9% and 8.1% respectively to $1.36b despite the higher win rate at 24.20%. Overall, MBS delivered an estimated adjusted EBITDA of $369.9m (+13.7% qoq, -32.7% yoy) while gaming EBITDA is estimated to be $349.4m for the qtr. On a notional hold-adjusted basis, 4Q12 EBITDA would have been up 6.9% yoy to US$406.4m (about $499m).

UOB Kay Hian highlights mixed implications for Genting SP. Note that while MBS' 4Q12 results suggests that GENS would also enjoy a relatively robust RCV for the same quarter, the quantum of recovery may not be as robust at GENS given MBS' low win percentage (a low win percentage could have allowed players to extend their play, which raises RVC). More importantly, MBS' figures point to a contracting mass market vol (noting that historically 4Q vol should have risen qoq instead of contracting in 4Q12), as local patronage continues to reel from tight rule enforcement by the Singapore government.

Still potential downside risk to GENS' 2013 EBITDA. Despite the surge in RCV and 4Q being a seasonally strong qtr, MBS delivered a property EBITDA of only $369.9m in 4Q12, -33% yoy. The falloff in mass GGR accounts for a significant portion of the earnings contraction, as the mass market segment commands a much higher margins than the VIP segment. While house reckon that the worst is over for GENS since posting an adjusted EBITDA of S$303m, its earnings recovery momentum may still be sluggish even after the opening of its Marine Life Park due to the contracting mass market segment. Hence, there could be downside to the 2013 consensus EBITDA forecast of S$1.45b.

UOB Kay Hian maintains SELL on GENS with a $1.10 based on a 10x EV/EBITDA target.

GLP

GLP: latest annoucement on the Company released, its Brazil JV delivered a 35k sm distribution centre in Brazil, which it is leasing to a leading global automotive corporation. The lease is for the first completed building at GLP Guarulhos in Sao Paulo. GLP Guarulhos will be constructed over a period of 4 yrs and will comprise 17 buildings with total GLA of up to 420k sm in total. The JV, GLP Brazil Devt Partners I was formed in Nov ’12, to acquire a portfolio of 5 devt projects in Brazil, in which GLP owns a 41.3% stake. GIC and the Canada Pension Plan Invmt Board own the remaining stakes.

Counter has also been up close to 40% over the past year, and the Street has a estimate TP of $2.88 on the Counter.

Innopac

Innopac: launches take-over bid for ASX-listed diamond miner, Merlin Diamonds, agreed to make an offer for 100% of the issued and paid-up share capital of Merlin Diamonds, at the bid price of A$0.28 (approximately 37% premium on the last closing price) for each Merlin Diamond share. The price translates to a total of A$59.4m (approximately $76m at an exchange rate of A$1.00 to S$1.28). With the acquisition, Innopac is poised to become the first and only listed diamond miner on the SGX-ST.

Merlin is the only diamond mine in Australia’s Northern Territory, with the second largest JORC-compliant diamond resource and reserve in Australia with 7.2m carats. Merlin Diamonds’ flagship project, Merlin Diamond Mine Project in Australia’s Northern Territory, is one of only three diamond mines in Australia and has a high proportion of gem-quality diamonds.

Although Merlin's FY12 sales generated proceeds of US$1.9m, Merlin had been in a loss in the past 2 years, with FY11 loss of A$1.3m, and FY12 loss of A$2.8m.

Innopac

Innopac: launches take-over bid for ASX-listed diamond miner, Merlin Diamonds, agreed to make an offer for 100% of the issued and paid-up share capital of Merlin Diamonds, at the bid price of A$0.28 (approximately 37% premium on the last closing price) for each Merlin Diamond share. The price translates to a total of A$59.4m (approximately $76m at an exchange rate of A$1.00 to S$1.28). With the acquisition, Innopac is poised to become the first and only listed diamond miner on the SGX-ST.

Merlin is the only diamond mine in Australia’s Northern Territory, with the second largest JORC-compliant diamond resource and reserve in Australia with 7.2m carats. Merlin Diamonds’ flagship project, Merlin Diamond Mine Project in Australia’s Northern Territory, is one of only three diamond mines in Australia and has a high proportion of gem-quality diamonds.

Although Merlin's FY12 sales generated proceeds of US$1.9m, Merlin had been in a loss in the past 2 years, with FY11 loss of A$1.3m, and FY12 loss of A$2.8m.

United Engineers (UE)

United Engineers (UE): CIMB gives its view on the WBL takeover offer by UE. House think the objective could be for the Lee-family to wrest control of WBL from STC. Wary of price weakness for UE if a bidding war pushes the offer above S$5.15, in house SOTP estimate of WBL. Meanwhile, maintain Outperform rating and TP of $3.59 (30% disc to RNAV), adding that UE is still a strong investment property play with potential for accretive divestments.

Add that there are limited synergies btwn UE and WBL, and offer could be a negative for UE if not for the relatively low valuations that WBL is trading at. UE’s offer is at a 19% premium to STC’s offer and 14% premium to the last traded price prior to STC’s offer announcement. House would not be surprised if STC comes up with a counter bid.

Think the objective could be to buy another 11.8% stake for majority control, worth $130m, is not a strain on UE’s balance sheet, while buying the remaining 61.7% stake would cost S$687m. House doubt STC will accept the $4 offer. Overall, cute that UE is still a strong investment property play (>70% of GAV) and see potential for accretive asset divestments and redevelopment of old assets. The stock in play is in no doubt, WBL

Del Monte

Del Monte: joins the Myanmar foray. Launches an exclusive range of international Del Monte pdts incl packaged fruits, tomato ketchup, pasta and spaghetti sauces in the Myanmar market. Del Monte partners with Global Sky Co, based in Yangon to distribute the pdts in Myanmar. By end of the yr, the Del Monte range of pdts will be available in mkts across Myanmar in Yangon, Mandalay and other key cities.

The stock trades at 20.2x P/E, 2.7x P/B.

Asiatravel

Asiatravel: Company announced the signing of an agreement with China Xinhua Travel Network Services Co. Ltd., which also owns travel site www.51you.com (http://www.51you.com), to supply its online wholesale system and to provide XML integration of its database with Xinhua Travel for a period of 3 years.

The online wholesale system; TAcentre.com, will be used by Xinhua Travel, which operates over 30 branches and over 400 retail outlets in all major cities in China, to book hotels, tours, attraction tickets and flight packages worldwide. As 51you.com enhances its online operating and distribution, Asiatravel will be supplying its global data of travel products seamlessly into 51you.com’s system.

OSK DMG has a BUY rating on the Company with a TP of $0.44.

Ausgroup

Ausgroup: Group announced it has been awarded an extension of their existing contract with Apache Energy Limited for ongoing works on Varanus Island and associated offshore facilities.

Valued at c.A$15m per annum, Group’s scope of works involves mechanical services, sheet metal fabrication, scaffolding and rigging and instrumentation and electrical services. Group will also provide minor capital works services including the fabrication and installation of pipe and structural work, roofing and wall cladding, painting and protective coatings, piping and, electrical upgrades.

Ausgroup has won several projects with a total contract value of A$50m this year, with a total order book at A$280m.

Ausgroup currently trades at 9x PE, vs peers Civmec at 20x, and Tat Hong at 15x.

STE

STE: The Group has been awarded a contract by the Ministry of Defence (MINDEF) for the design and build of eight new vessels. These new vessels will replace the Republic of Singapore Navy’s existing Fearless-class Patrol Vessels, indigenously designed and built by ST Marine in the 1990s. No further details could be released on the contract.

Design of the vessels will commence immediately and the delivery of these vessels is expected to be from 2016 onwards. The Group’s marine arm, Singapore Technologies Marine Ltd (ST Marine) will build the eight vessels at its Singapore Benoi Yard. Singapore Technologies Electronics Limited (ST Electronics), the Group’s electronics arm, will supply the core combat systems and combat system integration solutions.

MS previously noted that they are concerned about 1) weaker margin as the company ramps up new businesses; 2) lower earnings growth between 2012 and 2014; and 3) weakening USD affecting earnings. Valuation full at 19.8x forward P/E, more than 1 standard deviation vs. its 5yr avg of 16.9x.

MTQ

MTQ: 3Q13 rev +14% YoY to $36.6m, and registered growth across all business segments. Pre-tax earnings +51% YoY to $5.1m, but net profit, -34% YoY to $4.09m, due to a large one-off tax writeback in 3Q12.

DMG maintain Buy, TP $1.66, noting that 9M13 profits of $13.8m (+30% YoY) vs FY12 profits of $14.6m, supports forecast for a 32% jump in the bottom line to

$19.2m this yr. House encouraged by the margin expansion to 38.6% from 36.5% in 2Q13, a result mgt attributes to effective cost controls. MTQ is still only trading at 6.8x FY13F EPS vs other o&g plays which trade around 8x-20x.

SIA

SIA: Announced it will cut 76 pilots from its payroll by the end of June as part of cost-saving measures. The pilots, who are employed on fixed-term contracts, are being let go before the end of their contracts. SIA currently employs around 2,300 pilots. Note that SIA currently has a surplus of pilots to its operational requirements as the global financial crisis of 2009-10 had resulted in excess capacity and slower-than-expected growth. The airline had previously suspended cadet pilot recruitment and asked pilots to take voluntary unpaid leave.

Yoma

Yoma: Good set of 3Q13 results, which was broadly in-line, noting that 3Q12 was a very low base. 3Q13 rev at $13m, +32% yoy and net profit at $3.7m, +170% yoy. Gross margins jumped to 49.1% vs 25.7% yoy.

Rev was driven largely by the sale of residences in 3Q13, which increased more than threefold compared to the previous corresponding period. The increase in the sale of residences was mainly attributable to additional property dev projects such as Ivory Court Residences II, Bamboo Grove Garden Villa and new blocks of Lakeview Apartments at Pun Hlaing Golf Estate, as well as the apartments at Star City.

Going forward, grp expects its real estate business to continue to be the driving force for the foreseeable future and continuously look to increase its activity in real estate in Myanmar. At the same time continuing to grow and develop other business areas in agriculture and automobiles.

Tuan Sing

Tuan Sing: Posted a very strong set of 4Q results. (No Coverage on counter). Rev at $112m, +56% yoy and net profit at $79.m, +214% yoy. Result brings FY12 rev to $371.8m, +55% yoy and net profit to $109.5m, +172% yoy, which also included a fair value gain of $67.7m on investment properties. Profit before tax and fairvalue adjustments was +129% yoy at $56.2m.

Property rev was +365% to $188.3m, driven by sales from grp’s Mont Timah and Seletar Park Residence in Singapore and Lakeside Ville Phase III in China, inclusive of the fair value gain of $72.0m, Property contributed approximately 85% of the Group’s total profit for the year. Hotels Investment Grand Hyatt Melbourne and Hyatt Regency Perth registered a combined 13% growth in RevPar, as GHG reported a full year 10% increase in NPI to A$44.1m, but profit after tax of A$3.6m was lower than last year due largely to a net fair value loss recorded.

In grp’s other Investments GulTech recorded a 13% increase in rev to US$267.2m and a 62% increase in net profit attributable to shareholders to US$25.1m. This was driven by growth in the disk-drive, networking and consumer electronics sectors, improved margin and better sales mix, as well as a concessionary corporate tax rate granted recently by the local government to its Wuxi plant.

Going forward, grp note that 2013 is expected to be a challenging year particularly for the dev property business. In SG, Grp will continue marketing its remaining units at Seletar Park Residence and plans to launch Sennett Residence in first quarter 2013 and Cluny Park Residence this yr. Overall, barring unforeseen circumstances, the Group is cautiously optimistic of achieving satisfactory operational performance before fair value adjustments for the year 2013 Grp trades at just 0.6x P/B and has declared a final dividend of 0.5c per share.

SATS

SATS: 3Q13 results in-line. 3Q13 rev at $470.6m, +6.4%yoy and +2% qoq, and core net profit at $47m, +7.6% yoy and -7% qoq. Result brings 9M13 rev to $1.37b, +9.4% yoy and net profit to $139m, +7% yoy.

Results were led by increased flights and higher meal vol led to gateway and food businesses reporting a 6.8% and 6.2% growth in rev respectively. This was however dragged by higher Operating expenditure, +6.3% to $423.8m due mainly to higher staff, raw material and licensing costs incurred, in line with higher business vol.

Despite rising costs, the Group earned an operating profit of $46.8m, + 6.8% yoy, although Operating margins remained tight at 9.9%.

Share of results of associates and JVs, net of tax rose 31.5% to $12.1m. Going forward, grp remains confident on outlook, noting that Airlines are expecting demand for air travel to improve in 2013 but airfreight demand is likely to remain weak in the coming mths. SATS expects start-up losses for its new businesses in remote catering and cruise handling to continue in the next quarter as budgeted.

Amid the uncertain economic environment, labour availability and labour costs in SG are major challenges for Grp, although tip sector to be in a structural recovery with passenger vol expected to hold up steady in intra-Asia traffic with the new terminal in SG and the introduction of the LCCs in Japan, together with the Middle Eastern carriers also increasing their filghts within Asia in 2011 and 2012.

Ratings as follows:

CIMB Maintains O/p with $3.32 TP

Deutsche maintains Buy with $3.05 TP

CS neutral with $2.90 TP

Maybank maintains Hold with $3.03 TP

Citi maintains Sell but raise TP to $2.70

FNN / Thai Bev

FNN / Thai Bev: TCC Assets said its stake in F&N stands at 50.92% after further purchases in the stock market and more shareholders accepting its $9.55/sh offer. With majority control now in the hands of the Thai parties, the F&N offer has become “unconditional”. The deadline for the rest of the shareholders to accept the offer has been extended from 4 Feb to 18 Feb.

Analysts believe more shareholders are likely to accept the offer as it is the only bid on the table.

The market however is closely watching whether Japanese brewer Kirin, which holds a 14.8% stake in F&N, will sell its interests or remain a minority shareholder. Kirin commented that it will make a decision on F&N by 4 Feb, and "will utilize the option that maximizes value for Kirin shareholders". That the Board of F&N has referred to TCC's revised offer of $9.55/sh as "fair", and the directors intend to accept the offer with respect to their own direct shareholdings, may offer a hint as to Kirin’s final actions.

Thai Bev shares extended its price run yday, on expectations that the takeover of FNN appears all but assured. This may be a likely signal that investor interest has now shifted to the acquirer, and on anticipation that an effective an integration between TCC, Thai Bev and FNN could translate to synergies for the group.

Genting SP

Genting SP / Las Vegas Sands: First read through from LVS results indicate weak results from MBS in Singapore. 4Q12 adjusted EBITDA was US$302.5m, -29.1% yoy, as EBITDA margin tumbled from 52.9% to 42.2% yoy. The unfavorable impact was due to a significantly lower Rolling Chip win % of 2.14% from 3.34% yoy, despite MBS recording the second highest quarterly volume in its history at US$16.47b, +53% yoy. Other gaming statistics were slightly weaker, with non-rolling chip drop at US$1.1b, -3.2% yoy, and Slot Handle at US$2.7b, -2.0% yoy.

By extension, the market may express concerns about the possibility of a weaker showing at GENS. The higher than expected hold-rate volatility leads to larger EBITDA volatility, and may raise the equity risk premium on the Singapore gaming business.

Overall, LVS 4Q12 results topped analysts’ estimates, with despite profit being little changed. FY12 was a year of record earnings, led by growth in Macau, which saw a pick up in gambling. Macau revenue rose 48% yoy (vs Spore revenue of -11%). Adelson noted, he “couldn’t be more optimistic about the future”. Expect a renewed focus on Macau plays today, which could further take the shine away from Singapore-listed GENS.

Nevertheless, GENS is +3.4% at $1.515.

Swing Media

Swing Media: Positive news flow for grp, with grp announcing that it has clinched a deal to install solar-powered lighting for 300 PetroChina gas stations and signed a MOU to convert 200 more PetroChina gas stations.

CEO note that this is just the tip of the Ice Berg, as PetroChina has 50,000 gas stations across China. And there are another 50,000 stations owned by other state-owned and private players. Co. had so far installed solar systems for 20 gas stations in China, and would start work on the rest this yr, which will keep grp very busy for a while.

The profit per solar conversion project is about 100,000 yuan (S$19,860). For 300 projects, this translates into a potential profit of some $6m for Swing Media, which could double Swing Media's bottom line within the next two yrs. Add that the Chinese government has started getting very serious about energy conservation and pollution, and this emphasis has increased with the new government. In time, China expects to tap solar energy for much of its needs.

DMG has a Buy Call on the counter with a 0.24c TP.

SG Market (31 Jan 13)

SG Market: STI resistance at 3280, support at 3230.

Among stocks in focus:

*STATS – 3QFY13 results in line with expectations with revenue +6.4% yoy to $471m and core net profit +7.6% to $47m

*Tuan Sing – Strong set of results in 4Q12 with net profit jumping 214% to $79.1m, boosted by property development profits and $67.5m revaluation gains; DPS of 0.5¢. Stock trades at steep discount to NAV of $0.609.

*Yoma – Reports 170% jump in 3QFY13 net profit of $3.7m on 32% rise in revenue from Myanmar property projects.

*F&N – TCC Assets makes further share purchases and takes its stake in F&N to 50.92%, making its $9.55 offer unconditional, extends deadline for its takeover offer from 4 Feb to 18 Feb.

*ST Engrg – Wins newbuild contract for 8 naval vessels for RSN with first delivery in 2016; contract size not revealed for confidentiality reasons.

*Ausgroup – Secures additional A$15m per annum contract from Apache Energy

*Del Monte – Joins growing list of Myanmar stocks to distribute packaged fruits, sauces, pasta and fruits drinks in Yangon, Mandalay and other key cities in Myanmar by end 2013.

*SIA – Releasing 76 pilots on fixed-term contract pilots, citing pilot surplus on long haul flights, suggesting challenging times for the carrier.

Wednesday, January 30, 2013

Guocoland (technical)

Guocoland - Technicals looking good for more upside, with Stochastic and RSI both hooking upwards from OverSold territory. Counter is currently testing its 20 day MA at $2.33, and a close above these levels could see further upside.

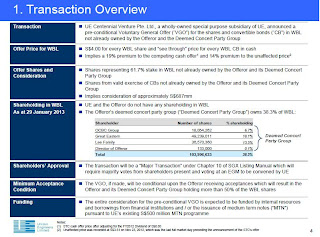

UE/WBL

UE/WBL: UE TO LAUNCH ALL-CASH PRE-CONDITIONAL VOLUNTARY GENERAL OFFER FOR WBL AT $4.00 A SHARE

United Engineers / WBL: United Engineers announced that it intends to launch a takeover for WBL in an all-cash pre-conditional voluntary offer that values WBL at close to $1.1b. The Offer is for the remaining 61.7% of WBL, or 167.6m shares, and all outstanding convertible bonds in WBL, that the Offeror and its concert parties do not own.

The concert parties comprising OCBC Bank, Great Eastern, the Lee Group, and directors of the Offeror, own a combined 38.3% stake in WBL. The Offer price at $4.00/share is at a 19.0% premium to a competing cash offer (adjusted for dividend) and represents a 14.0%, 13.3% and 12.0% premium to the last transacted price on 23 November 2012, 1-month VWAP and 3-month VWAP up to 23 Nov12, respectively.

UE said the rationale for the Offer is as follows:

1) To expand and diversify the UE Group’s development and investment property

2) Gain exposure to longer-term growth in PRC’s real estate market

3) Harness synergies, particularly between properties, construction, and

engineering businesses

4) Add additional growth engine via WBL’s automotive business, which is a

source of recurring income

5) Explore opportunities to enhance value across the WBL’s diverse portfolio of

businesses

Grp note that for WBL shareholders, Offer provides a better alternative at a 19.0% premium to a competing cash bid.

Recall 2 weeks ago, STRAITS Trading Co announced plans to buy 64.02m WBL shares, or 23.61% of the firm, from Aberdeen Asset Management Asia and Third Avenue Management. This will be paid for with the 68.5m new Straits Trading shares to be issued, in a share swap of 1.07 shares for every WBL share. The acquisition will bring Straits Trading combined holdings, together with parties acting in concert, to 44.6%. WBL shareholders will then have the option of receiving either 1.07 new Straits Trading shares or $3.41 in cash - the average price of WBL shares on Nov 23 - for each WBL share they hold.

We note that OCBC , which holds 5.84% of WBL, had expressed concerns then that the offer may be too low. It noted that the cash offer of $3.41 a share is below WBL's latest reported net asset value of $3.48 a share.

Thai Bev

Thai Bev: is up 10.1% at $0.545, a fresh all-time high, extending Tuesday's 8.8% gain as the takeover of around 29%-owned FNN by TCC Assets appears assured TCC Assets and ThaiBev are both controlled by Thai billionaire Charoen Sirivadhanabhakdi.

NRA says Thai Bev is the major shareholder of an "undervalued asset," believes Thai Bev will try to unlock more value in F&N. Expects the F&B business may be split into two vehicles, where there's probably more value, with other divestments a possibility. Says, the market is doing a sum of the parts valuation, but notes, "it's probably a one to two year story."

F&N is up 0.1% at $9.56, with the stock likely to remain penned near the $9.55/share takeover offer.

Stats Chippac

Stats Chippac: Counter is up 3% today, with the positive news flow continuing on. STATS ChipPAC and UMC Unveil World’s First 3D IC Developed under an Open Ecosystem Model.

Stats and UMC, a leading global semiconductor foundry, today announced the world’s first demonstration of TSV-enabled 3D IC chip stacking technology developed under an open ecosystem collaboration. The 3D chip stack, consisting of a Wide I/O memory test chip stacked upon a TSV-embedded 28nm processor test chip, successfully reached a major milestone on package-level reliability assessment. This success demonstrates a total solution for reliable 3D IC manufacturing through the combination of UMC’s foundry and STATS ChipPAC’s packaging services.

We like to highlight that newsflows regarding Stats Chippac has been pretty positive over the last few wks. Earlier this mth, Stats raised its 4Q12 sales guidance by between 9-14% on the back of better than expected demand from smart-phones and tablet computers. Capex budget was also raised between 20-40%. With its continued increase in capex spending, and proven R&D capabilities, the Company is in a good position within the Tech space.

UE/WBL

UE/WBL: Both stocks requested for trading halt pending anncmt. We hazard the possibility of a restructuring within the OCBC group as the bank holds direct and deemed interests (via Great Eastern) in both UE (19.4% stake) and WBL (24.8%).

At the sametime, WBL owns a 7.5% stake in UE and is subject of a conditional takeover by Straits Trading, which recently raised its stake in the company to 44.55% via purchases from Third Avenue and Aberdeen Asset Mgmt.

CDL Hospitality Trust

CDL Hospitality Trust - 4Q12 results were generally in line with consensus estimates. Revenue +1.4% YoY to $38.3m, and NPI , +0.2% YoY to $35.6m. RevPAR for the Singapore hotels was flat YoY in 4Q12 at $205 (excludes Studio M Hotel, which was acquired on 3 May 2011). FY12 DPU totaled 11.32c, +2.4% YoY and giving an annualised distribution yield of 5.7% based on the closing price on 29 Jan13. For 1Q13, management noted that apart from stiffer competition, there will be the absence of the bi-annual Singapore Airshow and additionally, CNY will fall later this year (Feb instead of Jan), possibly delaying the seasonal pick-up in corporate travel. Weaker accommodation demand by corporates and leisure travellers is likely over the next 12 mths. OCBC maintain fair value estimate of $1.93 and HOLD rating on CDLHT

HL Asia (technical)

HL Asia: Trading Central has technical Sell Call. HOuse note that the downside prevails as long as 1.76 is resistance. The RSI is below 30. It could either mean that the stock is in a lasting downtrend or just oversold and therefore bound to retrace (look for bullish divergence in this case). The MACD is below its signal line and negative. The configuration is negative. Moreover, the stock is trading under both its 20 and 50 day MA (respectively at 1.75 and 1.69).

Q&M

Q&M - Latest news on the co. was this mth, where grp announced the proposed takeover of Singapore Medical Grp. To finance the proposed deal, Q & M will mainly use proceeds from placement of shares, together with internal funds and current credit lines. The proposed deal is expected to create a regional healthcare group that offers comprehensive and holistic medical care from unique specialty, in line with the trend of increasing consumer expenditure on healthcare services, longer life expectancy among Asians and stronger purchasing power in Asia.

SMG currently operates 15 medical clinics in SG which are categorized into four medical clusters: Eye, Aesthetics, Orthopaedic and Sports, and Critical Illness. Both Q & M and SMG would be able to better complement its current businesses and operations through the sharing of resources such as premises, supporting staff and management, and enhancing the availability of specialty dental and medical care to their combined pool of patients. SMG currently has a patient database in excess of 80,000, while Q & M has more than 450,000 patients in its database.

Seperately note also that Q&M's main growth driver is China, where Q&M plans to invest RMB 400m to have 50 dental clinics and 20 laboratories by 2015 through JV’s mainly and, partly, its own Q&M dental clinics in Shanghai. Q&M is working on several JVs and targeting to achieve an aggregate profit of RMB 80m from China, and mgt has reiterated that it aims to seek an IPO for the PRC business either in China or Hong Kong in 3-5 yrs.

SingPost

SingPost: Continues its 52 wk high price, and moving towards the all-time high of $1.24 in Sept 2010. After CEO Dr Wolfgang Baier tookover in Oct 2011, the Company has been in a bid to improve efficiency and productivity.

Recall previous post with regards to its range of acquisitions:

SingPost has been making a list of acquisitions in recent months, mostly for mail and total logistics solution providers, spanning across the Asia region. In a bid of its transformation, the logistics business is expected to be a key driver going forward.

With the rise in online consumerism, it is no surprise that logistics solutions will be more in demand. Execution quality of the management has been proven given the quick inclusion of acquired companies over this period. As a yield play, SingPost has a dividend yield of 5.4% for FY12.

Midas

Midas: China infrastructure companies have funding secured for 2013. Recent reports stating China's plans to spend

Rmb650b on its railway system in 2013, including Rmb520b earmarked for building infrastructure. The total investment will be the third largest in the country's history after 2009 and 2010 and would extend China's rail network by 5,200km.

MoR took a bank loan on 45% of the funding, railway bonds made up 29% and funds from local govt and enterprises of 13%, with the remaining 13% of funding released on the central government budget.

Funding was an issue for the past 2 years amidst the misappropriation scandal, causing the entire sector overhang. Going forward, DB believe there is an upside potential on the railway spending budget through government support. This should translate to a healthy order flow for rail equipment makers like Midas.

After an earnings decline in GY12, the street is projecting EPS to bounce back strongly by 680% (albeit from a low base) in FY13 and 35% in FY14. The stock currently trades at FY13 P/B of 1.05x with a market ascribed TP of $0.55.

Golden Agri

CPO/Golden Agri: CLSA notes that CPO price likely to stay depressed below RM3,000/t average for FY13, due to the high stock levels and weakness in demand despite the festival season.

Record soybean crop expected in Americas are a key concern, as the spread between CPO and soyoil will likely close due to prices of soyoil coming down. CLSA reduce FY13 CPO forecast from RM3,000/t to RM2,600/t, and expect a recovery to RM2,800/t in FY14 once the excess inventory is run down.

CLSA maintains a BUY on Golden Agri despite the negative sector outlook, with a TP of $0.78. House is positive due to the potential upside from its trading team as well as M&A options from the money it has raised.

CapitaLand (technical)

CapitaLand: Trading Central note share price is strongly supported by a medium term ascending trendline, as well as the rising 50 day moving average, which should also limit the downside potential. The RSI remains well oriented and stands firmly above the neutral 50 level. As long as support at $3.85 is not broken, the house sees a further advance toward $4.14 and $4.23 (Oct ’10 high) in extension.

CMA

CMA: Deutsche notes CMA has stepped up activity in Japan in 2012, with the acquisition of 3 malls owned by 26%-owned CapitaMalls Japan Fund for $217m, and the purchase of Olinas malls for ¥22.8b ($367.3m). CMA’s Japan portfolio currently comprises 8 malls valued at ~$700m, located in Tokyo, Hokkaido and Osaka with 1.9m sf NLA.

CMA earlier commented that its strategy was to build critical mass, and it is exploring options (including a public or private REIT or fund) to create a Japan platform which would enable them to tap domestic capital and pension funds. This could take place over the medium term. A stronger presence will also strengthen the group’s ability to bring Japanese retailers into Singapore or China.

Nevertheless, with the stock trading at 1.3x P/B, at par to Deutsche’s RNAV of $2.18, the house believes valns look fair and maintains the stock at Hold with TP $1.96.

Indofood Agri

Indofood Agri: CIMB maintains O/p with $1.51 TP. House like Indofood Agri’s purchase of sugar assets in Brazil as the growth potential is compelling and the acquisition price is fair. The group expects its Brazil mill to raise its sugar production from 2.1m tons in FY13 to 3.8m tons in FY15. House also view the implied EV/tonne for the sugar mill capacity as fair, being within recent market transactions. Overall, maintain Outperform call and target price of $1.51, which is based on a 10% discount to its SOP value. Key re-rating catalysts are this acquisition and better CPO prices.

Yangzijiang

Yangzijiang: Seaspan, a ship-leasing unit of Tiger Group Invmts, may order as many as 15 more container ships over the next year to benefit from the lowest vessel prices in more than four years.

Seaspan CEO Gerry Wang, said it is in talks with two to three container lines to lease the ships it plans to purchase. The company had already ordered another 15 vessels from Hyundai Heavy Industries in the last three weeks, to be delivered from 2015.

Wang observes, “there’s always demand for modern ships and for fuel-efficient ships… Operators are getting more confident… more older ships [will be] phased out.”

Ship prices have dropped because of industrywide losses, overcapacity and tighter financing caused by European banks paring lending. The price of a vessel that can carry as many as 13,500 TEU containers was worth US$107m last month, the lowest since Jun ’08, according to Clarkson, the world’s biggest shipbroker.

Yangzijiang may be a beneficiary of more orders from Seaspan. YZJ currently has 11 firmed orders from Seaspan, for the 10,000 TEU containerships, 4 of which were options exercised last wk at a price tag of ~US$90m per vessel. An earlier order of 7 vessels was priced at US$100m per vessel. YZJ currently has 14 more options with Seaspan outstanding.

YZJ trades at 5.1x P/E, 1.3x P/B.

Mermaid

Mermaid: Announce that its units has been awarded a series of contracts from existing clients for the provision of subsea services to support offshore oil and gas fields in the Gulf of Thailand, Sakhalin and Qatar. The combined value of these contract awards is approximately US$30m.

The announcement follows a number of significant deals for Mermaid over the last few mths. In Oct12, 2 Mermaid associates concluded deals with Saudi Arabian Oil Co, for a US$530m inspection, repair, and maintenance contract and a US$235.5m jack-up drilling services contract. Meanwhile in Nov12 Subtech announced a US$25m contract with Total, a leading international upstream oil and gas company, utilizing the ‘Mermaid Siam’ in Qatar and last week MOS announced a US$30m subsea construction services contract award from China Offshore Oil Engineering Co.

We note that prospects for Mermaid appears more rosy then before, and in its latest Fy12 results, grp managed to register a turn around in its business operations, registering a net profit of Thb71.5m, vs a net loss of Thb167.3m yoy.

CIMB has an O/p rating on grp with a $0.44 TP

Singtel

Singtel: Company sold its entire 30% stake in Pakistan's Warid Telecom to the Abu Dhabi Group for $185m. Loss on disposal will be approximately $230m, including FX translation losses and transaction costs.

Bharti (contributes c.11% NAV to Singtel) has benefitted from the recent improvement in the competitive environment in India with two rounds of price increases since Nov 2012, with the exit of several smaller players. Indonesia's Telkomsel (contributes c.16% NAV to Singtel) is targeting stronger growth in 2013 as compared to the previous year, due to the lower mobile penetration relative to the region.

Singapore (c.29% NAV to Singtel) embarked on its tiered data pricing, with recent positive results from competitor M1 saw revenue growth improve on the take-up of the tiered data plans.

MS rates OVERWEIGHT on Singtel, with a TP of $3.80 based on FY13 15x P/E and a dividend yield of 4.9%.

Starhill Global

Starhill Global: Good set of results which was in-line, but at the top end of estimates. NPI at $37.6m, +3% yoy and +3% qoq and DPU at 1.13c, +11.9% yoy and +1.8% qoq. For the full year, NPI at $148.5m, +3.4% yoy and DPU at 4.39c, +6.6% yoy.

Grp note that results was boosted by the successful completion of the asset redevelopment work in Wisma Atria, coupled with the record-breaking visitor arrivals, which contributed positively to our Singapore performance. Wisma Atria retail average passing rent continues to scale from $35.04 psf/mth last quarter to $35.82 psf/mt.

Going forward, Starhill is propoposing to acquire the Plaza Arcade in Perth, Australia. Located in the prime shopping stretch in Perth’s city centre, which will be a valuable addition to SGREIT’s portfolio of quality assets in prime locations. The acquisition is accretive and being adjacent to reit’s existing David Jones Building, there are also potential synergies to be reaped between the two properties. Overall fundamentals remains strong, with gearing at 31% and occupancy rates at 99.4%. At current price, grp trades at 5.59% yield and 1x P/B.

Ratings as follows:

CIMB maintains neutral with $0.84 TP

Maybank-KE maintains Buy with $0.90 TP

Macquarie maintains Neutral with $0.76 TP

SMRT

SMRT: 3QFYMar13 results fall short.

Net profit at $26m, -31% yoy, -23% qoq, despite revenue rising 5% yoy to $281.7m on the back of higher fares and improved ridership trends.

Operating margins remain under pressure, in lieu of rising operating expenses in MRT and bus losses. Notably, staff costs rose 18% yoy to $98.5m, on account of increased headcount and higher basic salaries, while repair and maintenance expenses rose 29% to $27m due to the Circle Line and increased repair & maintenance schedule for trains, as well as a larger bus and taxi fleet.

Outlook continues to look cloudy, as mgt expects staff costs, depreciation and maintenance costs to continue to rise significantly moving forward. Mgt also expects capex to be significant in FY4Q, on the back of the takeover of operating assets in Changi and Dover, as well as train maintenance and fleet expansion.

At 17.1x fwd P/E, Deutsche believes valuation is only fair, given few near term catalysts. Keeps at Hold with TP $1.59.

Maybank KE sees no light at the end of the tunnel yet for SMRT, reiterates its Sell rating, and trims TP to $1.34 (from $1.37) to account for further operating expense increases. Advises investors looking for transport-related yield plays to consider switching to other sectors like aviation services where industry fundamentals present a rosier environment than that currently facing the Singapore land transport operators.

SG Market (30 Jan 13)

SG Market: S’pore shares are likely to open with an upside bias on the positive cue from Wall Street and the STI could rebound from a slight drop on Tue but gains may be capped at the 3280 resistance given the lack of earnings catalysts from recent results.

Among the latest corporate news, SMRT could face some selling prssiure after reporting a 31.2% drop in 3QFY13 net profit on higher expenses from increased hiring and salary adjustments. SingTel's sale of 30% stake in Pakistan's Warid Telecom may be a slight negative in the short-term, as it took a $230m loss on the sale. Starhill Global 4Q results was in line with expectations. MCL puts in a top bid for a Jurong West site.

Tuesday, January 29, 2013

52 wk highs

52 wk highs:

REITs -- MCT, Starhill Global

PROPERTY -- UOL , China New Town Devt

CONSTRUCTION & RELATED -- Chip Eng Seng, Keong Hong, Pollux , Tiong Woon, Lum Chang, Hafary, Engro , TTJ

CONSUMER -- Thai Bev, BreadTalk

BLUE CHIP -- SGX , Comfort Delgro

OFFSHORE & MARINE -- Baker Tech,

S-CHIP -- Tianjin Zhong Xin Pharma, Delong, Unionmet , Peoples Food

MYANMAR -- Ntegrator, Interra Resources

OTHERS -- Unionsteel, Hupsteel, Cosmosteel, Innopac, AEI, Annaik, Innovalues, SP Ausnet, CWT, Singapore Shipping, WBL, United Overseas Insurance, Ace Achieve Infocom, HL Finance

ETF -- United SSE 50 China , DB X-TR II AU Dollar CSH-2C, Lyxor MSCI Europe B, iShares Asia High Yield Bond, DB X Trackers MSCI World Trn, DB X Trackers S&P/ ASX 200 UC, iShares MSCI India Index

JES

JES: 39m shares translates to 3.3% of shares out. Add that with the 34.6m shares sold in early Jan, this translates to a combined 6.3% stake sold by the CEO within a period of one month.

The shares have risen ~67% from the low of $0.135 on Christmas eve, to the current $0.225.

Over this period, there were market whispers that JES might be an acquisition target.

However, if this were true, it would make more sense for the CEO to hold on to his majority stake in order to extract a control premium for his shares.

If we do not see a new significant shareholder emerge as a result of today's transaction, by contradiction, we can conclude that there is low probability that the rumors are true.

Valuation wise, JES trades at 0.67x P/B, below its larger peers Yangzijiang and Cosco at 1.3x and 1.7x respectively. Though conversly, JES trades at a higher 24.9x P/E, vs YZJ's 5x P/E and Cosco's 17.8x P/E.

Noble

Noble: Pinning down the financial impact on Noble from Argentina's move to suspend the company from a key grain registry for alleged tax evasion could be difficult; a person at Noble said the suspension wouldn't impact operations.

Maybank KE Research notes, Noble doesn't have a clear breakdown out of Argentina, although it exports grains and soybeans from the country. But adds, "it's not something that's company specific to Noble. All the other grain exporters have had the same setback, so we're not reading too much into it."

On whether disruptions at 13.2%-owned Yancoal's (YAL.AU) Queensland mines due to rainfall would affect earnings, the house notes it isn't a significant portion of profit. The bulk of Noble's 3Q profit came from the energy segment.

The stock is down 2.4% at $1.22.

SGX (technical)

SGX: technicals; An ascending triangle formation indicating accumulation is emerging on the Counter, which could signal further upside ahead. Support of $7.67 at the 20 MA, and resistance at $7.70. A breakout above $7.70 would see the Stock be supported at that level, and the uptrend to continue.

On the fundamentals that was highlighted- after its good set of results released recently, an estimated 20 to 30 companies are expected to launch their IPOs in SGX in 2013, with each of these companies having an overall market cap of at least $500m- bringing the potential raising of $10-15b in proceeds. Analysts on the Street have also been revising 2013/2014 earnings upwards in the past 4 weeks.

CWT (technical)

CWT: Prices set a new all-time high today at $1.415.

CIMB reiterated the stock as one of its Top Small-Cap Picks this morning, with a $1.68 TP.

Tianjin Zhong Xin Pharma

Tianjin Zhong Xin Pharma: expects to report about 70 - 90% yoy rise in net profit for FY12 due to gain on disposal of subsidiary, increase in the return on invmt and increase in operating profits from the group's main business.

The stock gapped up this morning, minting a fresh 52 wk high. Last done at US$0.81, +6.6%.

Ipco

Ipco: is placing 350m new shares at an issue price of 1.98 cts for each placement share, to raise approx $6.9m.

This compares with the counter's last traded at 2.3cts.

The net proceeds will be used for working capital and short term invmt purposes.

Technics O&G

Technics O&G - No reason to explain its drop today. Note that grp's boardmembers has just approved grp's resolution in its recent EGM. Key findings were as follows:

Technics O&G: Grp just concluded its AGM and key findings were as follows. Recall through open market purchases of Technics shares, Eversendai emerged as a substantial shareholder with a 13.85% stake in early Dec and is targeting to own 20% to become an associate and is able to equity account Technics' profit. To support Eversendai's move towards the 20% target, Technics has proposed to issue new shares amounting to 5% of its enlarged capital.

Assuming the share issue is approved, Eversendai still has to go to the open market to buy the shares it wants for it to hit its target 20% stake. Technics now fabricates and commissions topside modules for wellhead satellite platforms (WSP), but does not do the heavy jacket fabrication. OSK-DMG note that recently Technics bidding for full WSP contracts and then subcontracting the jacket fabrication to Eversendai. Further, Eversendai’s presence in Msia may be Technics’ entry point into the highly-lucrative Petronas capex budget. Note that Eversendai has highlighted its strong business contacts in the Middle East and its potential to pave the way for Technics to secure business in that region which Technics is not established in.

DMG has a Buy call on counter with $1.20 TP.

Moya-Asia

Moya-Asia - Grp annouced yesterday that that barring any unforeseen circumstances, it expects to be in a loss position for the 3-month financial period ended 31 Dec012 and consequently expects to report a net loss of up to approximately $1m for FY12, mainly as a result of an unexpected increase in project costs, which was due to design changes in relation to the Cambodia projects. Grp also announced that it is currently in discussions with IFC (a member of the World Bank Group) in relation to potential financing to partially fund the BOT Project. (Announced in 20th Feb 2012) The total cost of the BOT Project is estimated at approximately US$140m, as well as an additional US$20m for contingency purposes. Grp has requested SGX to extend its Rights trading period to 1 Feb13. An announcement of the revised timetable will be made by the Co in due course following confirmation of certain dates with relevant authorities.

Ezion

Ezion: DMG Insti has a sales note on the counter, with house still largely favouring the stock. Note that using a DCF model and ONLY FACTURING IN THE ANNOUNCED CONTRACTS, with an 8% discount rate (the rate they issued the perpetual notes at) house derive a current price of $1.66, v the spot price today of $1.80, so at this price, despite the run, you are still only paying for orders already won, and not for future orders.

House also factored in a valuation if they continue to keep winning contracts at the current rate. IF we factor in another 10 liftboats (US$ 1.1b worth of new orders) over the next 5 yrs, then we can easily get a price of $2.52 (40% higher than today) assuming that there is no rerating of the multiple (currently 8x PE) from the increasing cashflow generation nor from the continued earnings growth (96% this year).

Since Ezion issued their perpetual notes Sept last year, they have announced almost US$700m in new contract wins, US1.4b in the last 12 mths and more than US$2B since the first liftboat in 2007. Clearly demand is still growing for their products, and mgt have stated that they are targeting to expand their fleet to own 20 rigs (including JV’s) by 2014.

Last week Ezion were reported to be going to issue another US$40m in perpetual notes, but the issue has been postponed for the moment as the bankers believed that it would require an interest rate yield greater than 8%. Ezion are not desperate for the money, as they have enough free cashflow coming in that they can redirect it, until such time as the market is “less demanding” (there had already been several successful issuances just prior already, and a problem with a Chinese perpetual which spooked the market but should not have had any effect on Ezion). They also still have the option of a sale and lease back on the various liftboats that they own, which is much more economic on a risk adjusted basis.

To put things in perspective, house also modeled up a scenario where they did issue them at a rate of 8%, and then announced the successful tender for a service rig, along the same lines as the recent contract that was announced in November, for delivery in 2014. This contract, despite the higher debt costs, further added another 18c per share to the valuation. Whilst they may not need the money, given the IRR in excess of 30%, each contract win is extremely profitable, even at a rate over 8% interest cost.

Technically speaking, Ezion looks to be consolidating after a very strong run around the $1.80 level. House will be a big buyer into any pull back as the guaranteed earnings growth to come through, not just this year (96%), but in 2014 as well (35%+) mean that you get an unusual level of certainty. Will continue to buy with a break of $1.90 with volume increase, or below $1.65 for a pull back. Use a break of the $1.55 level as a stop.

Noble Group (technical)

Noble Group: Technicals; Stock continues to rebound off key chart support at the $1.00-$1.02 area. A clear double bottom pattern is at play. A break above $1.37-$1.40 would trigger the bullish implications of the double bottom pattern. The strength of the current strength is strong at 26 ADX, and immediate support at the 20 MA at $1.225.

CNMC

CNMC: Company announced its 81%-owned subsidiary CMNM Mining Group has entered into a Technical Services and Co-operation Agreement for mine development and technology consultation on gold production expansion with China Gold Guizhou Jinxing Gold Mining Industry Co., Ltd, a subsidiary of China National Gold Group Corporation (China Gold), on 26 January 2013.

China Gold is China’s largest gold producer and a state-owned enterprise. China Gold specialises in the extraction of non-ferrous metals which include, amongst others, gold, silver and copper, and covers operation from the upstream exloration to downstream product refining.

China Gold will assign a qualified and experienced mine superintendent, mining engineers, production engineers specialising in gold heap leaching operation, as well as mine laboratory technicians to CNMC’s Sokor Gold Project located in Kelantan State of Malaysia. The China Gold team, with its wealth of experience, will add-on and complement CNMC’s current on-site production team to manage, plan, design, construct, and oversee CNMC’s gold production expansion program for a 1-year period beginning from 1 Mar 2013 to 28 Feb 2014.

China Gold's mgmt stated that CNMC Goldmine’s Sokor project has immense potential both in terms of gold production as well as its resources and reserves, and they are confident that with the addition of their technical inputs, they are able to uplift the total output beyond CNMC’s current plan. Additionally, China Gold also hope to be able to work with CNMC beyond the current Sokor project.

Street estimates CNMC with a TP of $0.80, a potential upside of 72%.

Cosco Corp

Cosco Corp: Secured 2 vessel contracts worth $54m and to be delivered 1Q15, with construction on vessels are effective 28 Jan 2013. 2 Platform Supply Vessels worth US$54m in total, with an option (within 6 months), for another 2 contracts of similar vessels.

Parent Company Cosco Holdings posted a profit warning for 2012 yesterday, mainly attributing it to the weak international shipping market, which is within market expectations. If Group records another big loss in the year ended FY12, the Counter will be specially treated, and be placed a daily volatility restriction of +-5%, and also face the possibility of delisting.

Street's TP is at $0.73, signifying a downside of 24%.

Sheng Siong

Sheng Siong: OCBC downgrades to Hold with $0.55 TP. Note that despite having no significant developments since house last update report issued on 10 Dec 2012, Sheng Siong Group’s (SSG) share price has soared by more than 25%. View this amazing appreciation as a result of the street finally factoring in SSG’s successful store expansion phase last year, and is playing catch-up by raising its expectations

for the company ahead of its FY12 results release.

Add that SSG closed out FY12 with 33 stores (Gross Floor Area: +50K sf to 400K sf). SSG is ontrack to at least match its best net-profit performance back in FY10, which included a $9.4m gain from investments. Although its 4Q12 will experience a decline due to seasonal weakness and year-end stock count, do not expect a stock count writeoff of last year’s magnitude (a $1.7m inventory write-off reduced gross profit

margins by 1.2ppt).

Even after fine-tuning DCF model, fair value estimate only increases slightly to $0.58 from $0.55 previously. Therefore, house downgrade SSG to HOLD on valuation grounds. While house continue to favour the

co’s management and its growth prospects, its recent price action has been far too exuberant and unsustainable (TTM PE of 33x). Recommend investors take some profit around current levels, and wait patiently to re-enter at lower levels around $0.55.

Triyards

Triyards: UOB Kay Hian initiates Coverage with Buy call and $1.11 TP. HOuse note that Triyards is a proxy to the growing acceptance ofliftboats internationally, being one of the few yards outside the US capable ofbuilding such vessels. Forecast 3-year core net profit CAGR (FY12-15F)of 19%, excluding lumpy profit contribution from Ezra’s deepwater multi-layconstruction vessel Lewek Constellation. Add that Triyards is a proxy to the growing acceptance of liftboats internationally, being one of the few yards outside the US capable of building such vessels.

Believe the market in Southeast Asia, the Middle East and West Africa will be able to absorb 30-50 additional liftboats over the next 2-3 years, given that the ratio of liftboats to platforms in these regions is still relatively low at 1:106, compared with 1:26 in the GoM. Triyards will embark on further growth by: a)developing proprietary third-generation liftboat designs, b) expandingship repair capacity, c) diversifying into new products such as highspeedaluminium commercial and patrol vessels, and d) growing itsequipment business and branding.

Sino Grandness

Sino Grandness: As Sino Grandness is in the midst of preparing for a separate listing of their fruit and vegetable juice business (Garden Fresh) by 2014 (either in HK or Taiwan), Lim & Tan does a comparative valuation with similar co’s listed in HK/ Taiwan, based on grp’s consensus earnings, which street expects to rise 34% in 2013 to Rmb329m and about 50% of it is derived from Garden Fresh, translating to Rmb165m.

While much bigger in size than Sino Grandness, comparable co’s such as Uni President, Tingyi and Want Want are all trading at an average P/E of 25x 2013 earnings.

Assuming we take a 60% discount (10x PE) due to its smaller size, Garden Fresh alone would command a market cap of $330m ($1.24 per share) vs Sino Grandness’ current market cap of $228m ($0.86).

Sino Grandness’ current market value of $228m is only valuing the entire co at 3.5x 2013 earnings. While its share price has risen a significant 72% since Dec 12 and is currently at its all time listing high, its continued low 2013 valuation suggests that if the co is successful in listing Garden Fresh in 2014, it remains cheap even at this level.

Hyflux / Sound Global

Water & Environment / Hyflux / Sound Global: SCB has sector report. House note that the outlook for stocks in the waste, water and environment sectors should improve, aided by recent positive policies in relation to the sector.

China’s Ministry of Environmental Protection issued guidance for the 12th Five Year Plan (2011-15) with estimated 30% annual growth in the markets for environmental protection, including treating solid waste, wastewater and sludge, and de-sulphurisation and de-nitration.

Add that more projects in environmental protection could materialize in 2013, especially in waste-to-energy (WTE), which still lags behind the central government‘s target for 2015, and is poised to grow at a 28% CAGR during 2011-15. Pricing liberation is also progressing after years of stagnant development, as several municipal governments have started charging solid waste treatment fees, collected from residents through tap water suppliers.

Recommend that investors accumulate on weakness as long-term thesis is intact. Wastewater treatment is becoming increasingly competitive but rising tariffs maintain project IRRs. In this segment, ike Beijing Enterprises Water, followed by China Water Affairs. House has an O/p Rating on Sound Global with $0.86 TP & In-line on Hyflux with $1.70 TP.

AIMS AMP Capital Industrial REIT

AIMS AMP Capital Industrial REIT (AAREIT): is investing $25m to redevelop its Defu Lane 10 property, which will treble the value of the asset to $42.6m from $12m currently.

AAREIT’s gfa will be more than doubled from 97.4k sf to ~202.9k sf.

Highlights investment "will provide high returns, with the redevelopment profit margin expected to be ~14%".

The counter trades at 1.1x P/B, offers 6.5% yield.

Ascott Residence Trust (ART)

Ascott Residence Trust (ART): private placement of 114.9m new units (10.1% of existing shares out) at $1.305 per unit, to raise gross proceeds of $150m.

The new units represent 10.1% of existing shares out, and are issued at 8.1% below the last counter’s close at $1.42. Indicative pricing for the new units were at a price range of btwn $1.305 to $1.335 per unit.

The proceeds will be primarily used to fund potential future acquisitions, finance asset enhancement initiatives, repay existing debt and for general working capital.

Assuming the proceeds are used to pare existing debts, ART’s aggregate leverage will drop from 40.1% to 34.9%.

In conjunction with the private placement, ART will declare an Advanced Distribution from 1 Jan ’13 to the date immediately prior to the date of issue of new units. The Advanced Distribution is estimated to be between 0.59 cts and 0.63 cts per unit. The new units are expected to be issued on or about 6 Feb 2013.

DBS, Stan Chart are arranging the sale.

ART trades at 1.05x P/B, 6.0% yield.

Keppel REIT

Keppel REIT: On 26 Sep 2012, Keppel REIT announced the acquisition of a 50% interest in a new office tower to be built on the site of the Old Treasury Building in Perth, Western Australia. The Company announced yesterday that the Western Australia (WA) State Government has approved Mirvac Group’s sale of a 50% interest in the new office tower which will form part of the Treasury Building development in Perth. With the approval, Keppel REIT is on track to complete the acquisition of the office tower in Mar 2013.

Keppel REIT currently owns 3 quality office assets in the CBDs of Sydney and Brisbane. Perth CBD market is one of Australia’s tightest office markets with a limited pipeline of future supply and is underpinned by the state’s diverse resources-driven economy.

Company is currently trading at 1x P/B, 5.8% dividend yield with a gearing of 42.9%.

Stats Chippac

Stats Chippac: Positive newsflow continues, as grp announced that it has signed adefinitive patent license, settlement agreement with Tessera; results in dismissal of all claims, counterclaims between Tessera Inc, STATS ChipPAC and subsidiaries. This effectively ends all outstanding litigation between parties & Provides STATS ChipPAC and subsidiaries with 5-yr license to Tessera’s complete patent portfolio for semi packaging tech

We like to highlight that newsflows regarding Stats Chippac has been pretty positive over the last few wks. See our recent repost below as well:

Positive news flow continues for Stats, Spreadtrum Communications (SC), a semiconductor provider in China for smart-phones, and other consumer electronic products that support 2G, 3G and 4G wireless communication standards, has adopted STATS’ next generation Embedded Wafer Level Ball Grid Array (eWLB) packaging technology. SC said that STATS’ eWLB allows their products to have better performance, a more compact form factor and is also competitively priced.

The latest contract win demonstrate STATS’s capabilities in commercializing its cutting-edge wafer level packaging solution, helping Spreadtrum to offer increased performance and compact form factor at a competitive cost for the fast-growing China smartphone market.

Recall few days back TSMC, the world’largest foundry (metal castings) and a key customer of STATS reported 4Q12 sales, +25% yoy to NT$131b, beating expectations and also guided for 1Q 13 sales of NT$127-129b also beating expectations of NT$124b.Grp's founder and Chairman add that the co will be increasing their capex plans for 2013 by 13% due to stronger than expected demand for smart-phone and tablet computers. Earlier this mth, STATS too raised its 4Q12 sales guidance by between 9-14% on the back of better than expected demand from smart-phones and tablet computers. Capex budget was also raised between 20-40%.

Biosensors

Biosensors: Possible positive sentiments after grp note that it has achieved CE Mark approval for its polymer-free drug-coated stent (DCS), BioFreedom™. The trial will provide additional data to support the launch of BioFreedom in select markets during 2013. The full commercial launch is currently anticipated during 2014

Meanwhile, CIMB had a report out on grp, maintaining its O/P Rating with $1.75 TP. House note of investors concerns that the effects of lower licensing fees in Japan could linger on in 3Q13, and if the Japanese yen weakens further, BIG may begin to feel the pinch. Japan accounts for about 19% of its revenue.

However anticipated pricing pressure in the Chinese DES market has been milder than expected. Understand that since the 2 hospital tender exercises in Gangsu and Zhejiang provinces, things remain in status quo. Despite possible pricing pressure in the Chinese DES market, the vol growth alone in China and gross-margin advantages could bring BIG’s net margins back to the low-mid-30s.

Add that with grps recent fund raising exercise last week, a $300m 4.875% fixed-rate note due 2017, believe a substantial accretive acquisition could be in the making. The US is still missing from BIG’s atlas. With North American holding 56% of the global DES market, BIG hopes to secure its footing there eventually. House do not rule out strategic partnerships with established players, though acquisitions will give BIG an immediate footprint in this particular market.

Olam

Olam: share price may see some uncertainty, after the Commonwealth Bank (CBA) warns that Queensland may see some cotton crop losses on flooding, with the worst inland flooding through the Darling Downs region where production losses are likely. CBA adds, heavy rainfall is also widespread in parts of New South Wales, with most of the state’s cotton crops expected to benefit from the additional moisture, although there will be some exceptions.

Olam, via Brisbane-based Queensland Cotton, has access to about a third of the cotton crop in Australia, the world’s No. 4 shipper of the fiber, based on 2007 data.

Noble

Noble: Grp was suspended from Argentina’s Grains Register for an investigation into unpaid taxes, a local tax agency official said. Noble was removed from the register

because of an undisclosed amount of false invoices and potential use of third-party accounts. While suspended, Noble must pay a tax rate of 25% to export grain, up from a previous 10%.

Noble Argentine unit President said in an interview that the grp have no comments to make as they are buying grains and exporting grain as they do in any other business day.” Argentina’s tax agency, known as AFIP, last year said four of the South American country’s 10 biggest exporters and grain and soybean processors underpaid taxes and it would pursue full repayment. The

Noble exports between 4m and 5m mt of grain from Argentina annually, Romero said. The country’s total grain production was 90.9m tons for the 2011/2012 season. Bunge, Argentina’s second-biggest exporter, was suspended on Oct. 1 and excluded on Oct. 26 because of unpaid income taxes since 2006. Bunge remains suspended from the register.

Note that Argentina is the world’s largest exporter of soy oil, the second-largest of corn and third of soybeans. We note that Noble’s oilseed crushing plant, is situated at the port terminal of Timbúes in Argentina’s Santa Fe province, capable of producing 2.7m / mt of soybean oil, meal and pellets annually, the facility is a key contributor to Noble’s network of strategic crushing facilities, providing, substantially adding to Noble’s competitive advantage in worldwide oilseeds distribution.

Ascendas Hospitality Trust

Ascendas Hospitality Trust: 3QFYMar13 results above estimates.

DPU was 1.77 cts (with sponsor waiver), above prospectus forecast of 1.69 cts, because of lower than expected expenses.

Operationally, the performance of the Australian hotels was weaker than expected, with RevPar of A$129/day, -4% qoq and against the A$139/day prospectus forecast (-7%). Demand was weak due to ongoing refurbishments and the softening economic environment. However, margins continued to surprise in China and Australia. Mgt expects RevPar to pick up in Australia in FY14 after the refurbishments are completed.

Mgt remains on the look-out for more assets in its three existing operating markets as well as Singapore, HK and South Korea. Stan Chart believes AHT will follow its sibling A-REIT’s model of strong inorganic growth – AREIT grew its AUM by more than 3x within the first two years of listing. AHT’s leverage was at 35.8% as of 31 Dec 2012; it has $75-180m headroom before reaching a leverage of 40-45%.

With AHT trading at 1.3x P/B, 7.1% FY13e yield, Stan Chart believes current valns do not price in organic growth. Reiterates Outperform, lifts TP to $1.05 from $0.99.

SG Market (29 Jan 13)

SG Market: S’pore shares could open a tad higher despite cautious lead from Wall Street as traders take a breather from multiple sessions of gains. The STI is likely to make a slow and steady push towards next resistance at 3280, last set in Jan 11 with 3220 providing underlying support.

Among stocks in focus:

*Biosensors – Receives CE Mark approval for its polymer-free drug-coated BioFreedon stent

*Noble – Suspended from Argentine grain register on tax probe

Olam – Queensland cotton crop may be hit by floods but those in New South Wales may benefit from additional mositure

*Ascott Residence Trust – Raising $150m from private placement of 114.9m new shares @ $1.305 with proceeds used for potential acquisitions, debt repayment and working capital

*IndoAgri - Makes 1st foray into Brazil with 143.3m real acquisition