Friday, August 31, 2012

Key Beneficiaries of the Thomson Line

Key Beneficiaries of the Thomson Line:UOB Kay Hian has a very useful report on the Key Beneficiaries of the Thomson line. House identifies key listed beneficiaries as City Developments, Keppel Land, OUE, GuocoLand, UOL, UIC, SingLand, Frasers Centrepoint Trust, Starhill Global REIT and Wee Hur.

House tip residential developments along the line to see 5-10% gains. New developments

with unsold units include City Developments’s Up@ Robertson Quay, Keppel Land’s Marina Bay Suites, UIC’s V on Shenton, UOL and SingLand’s Bright Hill Drive site. The resale prices of developments will see modest 5-10% gains.

Retail REITs will benefit from increased shopper traffic. Causeway Point, which is owned by Frasers Centrepoint Trust, will be a key beneficiary as the Thomson Line will enhance connectivity to Thomson and Lentor, bringing greater shopper traffic. Orchard malls such as Wisma Atria and Ngee Ann City, which are partially owned by Starhill Global REIT, will benefit from improved connectivity to Northern Singapore.

Office developers to see improved office demand. New upcoming office developments by GuocoLand (Peck Seah Street site), Keppel Land (Marina Bay Financial Centre Tower 3) and OUE (DBS Tower upgrade and retail podium development) will see improved tenant demand on the back of improved connectivity to their developments.

Industrial developments in Woodlands to see higher take-up. Industrial developments in Woodlands by OKH (Primz Bizhub and Woodlands Horizon) and Wee Hur (Harvest @ Woodlands) will also see higher take-up from SMEs and industrialists.

CEFC Intl

CEFC Intl: Co recently changed its name (now China Energy Force Corporation) from Sun East and also its business to the trading of petrochemicals and fuel. So far co has not acquired or propose to acquire any business yet and as of 6 Aug had negative equity of $4.9m. Effectively a bankrupt co.

However it might be used as a backdoor listing through a reverse takeover. Given the official name change and business change, something might be brewing. Normally in an RTO, existing sh/h are massively diluted although they may obtain some value esp in cases where the net book value or equity is already negative.

K1 Venture

Latest update is that the offer has received acceptances representing approx. 76.08% of issued shares. (Below the 90% threshold required to take the CO. private)

Recall that the grp plans to delist the co, although a few analysts have advised against shareholders in accepting the deal, citing that K1 Ventures investments are starting to mature, and that the offer price does not reflect the true intrinsic value of the value of its investments.

So based on the current situation, while shareholders could get to hold on to their shares, but the company stocks could become more illiquid (In come cases, to the point it is as good as a private company)

Ascendas REIT

Ascendas REIT: Mapletree Log Trust, Cambridge and Ascendas REIT are their 52 wk high. Seems that the industrial REIT sector might be seeing some inflows. This could due to the higher yield and more defensive nature of REITs.

Ascendas also entered into a sale of its property Block 5006 Techplace II to Venture Corp at $38m. Was highlighted by us a couple of days ago. This will lower DPU by 0.01c but shld be at a favourable sale price given the offer was unsolicited.

UE E&C

UE E&C: Our in-house issues a bullish unrated note on co. Highlights that it has net cash position of 81% of its current mkt cap and trades at ex-cash PER of 2.2x and P/B 0.95x. Although co does not have a dividend policy, if based on last yr's payout, div yield would approximate 11%. UE is also 20% owned by OCBC which appears to be in divestment mode.

Report appears to be moving counter which is up 4.5% currently

Parkway Life REIT

Parkway Life REIT: CIMB downgrades to Neutral from Outperform but ups TP to $2.11 from $1.96 on a co visit.

Mgmt entered Msia through a small $6.5m acquisition completed in Aug 2012. House expects further acquisitions of Msia hospitals and believes total of $200m of acquisitions will provide DPU uplift of 0.4%. 2-4% min FPU growth is estimated on CPI-pegged leases of Sg hospitals (60% of rev) alone. Plans for Japan include AEI collaborations with the operator and appears to be a compelling strat for LT growth. House continues to like co for its defensiveness and see it as a good yield-play complement to IHH’s growth story (IHH owns 36% equity interest in Plife REIT), but at 30% premium over book and yield compression to 5%, upside appears limited.

Fortune REIT

Fortune REIT: In Jul, the HK retail sales climbed 3.8% YoY by value, significantly lower than the median 9.0% forecast of economists surveyed by Dow Jones Newswires and the YoY increases from Jan-Jun, which varied between 8.7% and 17.1%. A government spokesman attributed Jul's slow growth to the external economic environment and more cautious local consumer sentiment. Retail sales growth could be more moderate in 2H12 than 1H12 and this will reduce the extent of possible rental increases.

A new visa policy to be implemented starting 1 Sep will help more mainlanders travel to HK. OCBC estimate that mainland arrivals account for only 19% of HK retail sales, so any increase in retail sales due to the visa policy will likely be moderate. For suburban mall operators like FRT, local consumer sentiment will still be a more important driver for positive rental reversions. House maintain fair value of HK$5.33 and HOLD rating.

Interra Resources

Interra Resources: Goes ex-rights today. Theoretical ex-right prices based on yesterday's closing is at $0.33. Counter currently trading at $0.355 already. Recall, Yoma's share price shot-up the day after it went ex-rights few mths back.

F&N / ThaiBev

F&N / ThaiBev: UOB Kay Hian note that the potential final twist could be a struggle for F&N itself as ThaiBev’s stake in F&N of 29% is within a whisker of the 30% mandatory general offer level. House believe 2 scenarios could pan out in the near term. However, think these two near-term scenarios will subsequently lead to other developments later as a potential break-up of F&N cannot be ruled out. The near-term scenarios are:

1) F&N shareholders accepting Heineken’s final offer of S$53.00/share for APB, thus leading to the privatization of APB.

2) F&N shareholders reject Heineken’s final offer, maintaining the current status quo and incurring a break fee of $55.9m

For Thai Bev, the clear target would be APB given the direct synergies and the fact that F&N, excluding APB, would largely derive its value from property. Under this scenario, F&N may not be strategic for ThaiBev unless it plans to venture into property development.

As for Kirin, believe Kirin could be persuaded to support F&N’s board to sell APB to Heineken. See possibilities to entice Kirin including an offer of a first right of refusal by F&N to Kirin should F&N decide to dispose its non-alcoholic assets. In addition, confidence of F&N’s mgt to secure shareholders’ approval is apparent since it has provided a “break fee” clause of $55.9m to Heineken.

Valuation: Assuming F&N shareholders accept Heineken’s bid, follow up would be 1-for-3 capital reduction exercise for F&N. Under scenario, estimate RNAV of $10.40/share. After apital reduction exercise, more than 80% of its RNAV will consist of property-related assets. As such, mkt may impose higher discount of 15-20%, which will see F&N at $8.30-8.85/share.

However, should F&N’s shareholders reject Heineken’s bid, estimate a RNAV of $9.76/F&N share. Under this scenario, think a lower discount of 5-10% may be imposed given a lower proportion of property assets as a total of F&N’s RNAV (55% of total RNAV from property). Based on a discount of 5-10%, the potential valuation range should FNN not dispose APB would be $8.80-9.25

Mermaid

Mermaid: Announced that its subsidiary, MTR-1 has secured an accommodation barge support services contract with a potential value of US$5m. Contract was awarded by an existing client - an international upstream oil and gas company - and is for a duration of five months in Indonesia. MTR-1 is currently in Indonesia performing accommodation barge support services for the same client in a contract scheduled to end in Sept12. This new contract will commence back-to-back with the company's existing contract for the MTR-1.

We note that could be another potential turnard co. after the grp recently posted an improved set of 3Q12 results which saw rev at Thb 1.75b, +20.5% yoy and net profit at Thb 138.5m, +194.2% yoy, attributed to higher rev for grp's subsea segment which increased by 18.7% YoY due to utilisation rates and average day rates remaining stable YoY. Grp’s Drilling segment also reported rev of Thb 318.1m, an increase of 30.0% YoY due to MTR-1 resuming operations as an accommodation barge post its special periodic survey.

Note that the recent M&A transactions in SG has been largely attributed/linked to Thai Co's. E.g Sakari (PTT) and Thai Bev. Hence, do not rule out market playing on a similar theme regarding Mermaid, with 66% of grp’s shares in control by its Thai shareholders.

Saizen REIT

Saizen REIT: Divest building Rise Kojo Horibata to independent private investor for $1.4m. The building contributed abt 0.2% and comprises 12 residential units and 6 car parking units.

Otto Marine

Otto Marine: Secured long-term charter for Landing Craft. The contract is expected to be worth US$15.1m for the min scheduled period and up to US$18.5m with options. The charter is to support a world-class O&G major for construction and drilling works in Western Australia.

City Dev

City Dev: Clarifies article “CDL to sell huge Kranji industrial plot for $240m" in Business Times. Sale of land is a joint sale with subsi of Hong Leong Invt not City Dev alone. Of the $240m $150.8m is payable to Hong Leong's subsi and $89.2m to City Dev's subsi, both which are wholly owned. The completion of sale is scheduled on the 31 Oct 2012.

Suntec REIT

Suntec REIT: Announced that it is in no rush to lease out space which will be vacated by Carrefour, as the area will be undergoing a major revamp in early 2013. Add that areas occupied by Carrefour, the Rock Auditorium, Eng Wah cinemas and NUSS Clubhouse will also be vacated early next year to make way for new entertainment and lifestyle offerings, including a new cineplex. Phase Two of the renovation works is expected to be completed by end-2013.

Experts added that the landlord could also divide the large premises into smaller units to enjoy higher rentals, although the downside is that they could have many tenants to manage and there is also a vacancy risk.

SG Market (31 Aug 12)

SG Market: S’pore shares are set for a nail-biting month-end as players get cold feet after the Wall Street tumble as expectations fade that the Fed will announce new stimulus at the Jackson Hole meeting and may instead pin hopes on the ECB meeting on 6 Sep. Traders will be watching If the STI can hold above the key psychological support at the 3000 level with the next line of defence at 2975. Upside resistance is now set at 3030. A dearth of fresh corporate news may help keep players sidelined.

Mermaid Maritime landed a US$4.8m accommodation barge contract. Otto Marine deployed a Landing Craft in Australia on a long-term charter contract for US$15.1m. Osim bought back 450,000 shares at $1.257 in the open market. SIA’s budget carrier Scoot will add 3 more Chinese cities to network. Noble and Olam have been included in Forbes Asia's Fab 50 list.

Thursday, August 30, 2012

Aussino

Aussino widened its losses to $13.2m in FY12 from $5.3m the previous year on a 10% drop in revenue due to higher rental and labour costs, which rendered its stores in China unprofitable. The group closed more than 20 stores and cunters in China and ended its retail operations in HK and Korea, as well as incurred a $1.4m goodwill impairment charge for its ladies fashion business in Australia. Moving ahead, it will be adapting its business strategy to focus on distributorship and group sales in China. As of Jun 12, NAV stands at 2.8¢ per share, a sharp drop from 7.4¢ in FY11.

However, there is no relevance in looking at past Aussino’s performance anymore as the company is disposing its existing business to its parent and acquiring the energy business unit of Max Myanmar (owned by U Zaw Zaw) via a reverse takeover for $70m. Max Myanmar currently operates 21 petrol kiosks stations across key cities in Myanmar, storage facilities and an oil trading business and reported a $5.2m profit in FY12. Bear in mind that the proposed acquisition and RTO deal is still in progress pending approvals from shareholders and SGX and U Zaw Zaw is on the US sanctions list.

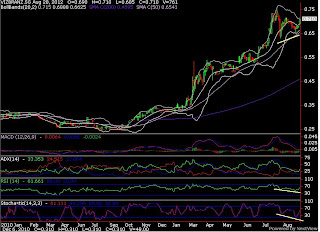

SP Ausnet (technical)

SP Ausnet: Stochastics and RSI are all trending upwards, which could signal further upside ahead, while counter is currently aboves its 20,50 and 200day EMA. Next resistance could be at the trend resistance of $1.38 or the recent mths high of $1.39.

Singtel

Singtel: UOBKH issues update, maintains Sell with TP$3.22. 32% own Bharti Airtel faces regulatory uncertainties which will affect its future earnings. The 2G auction has been delayed again for the 2nd time and the outcome will affect the future pricing of spectrum in India. This does not directly affect Bharti though. However Bharti is under investigation for excess spectrum allocated to it.

Bharti will also be affected by the refarming of 900MHz to 1800MHz spectrum when the existing licence expires in 2014-16. The 900MHz spectrum is more efficient and the refarming will result in additional capex for Bharti. The 900MHz spectrum freed by refarming will be allocated in a new 900MHz auction to be conducted as early as 1H13. The price will be set at 2x the 2G auction mentioned above.

Privatization plays

CIMB looks at potential privatization plays and tips STI at 3340, with an Overweight rating on Singapore. Note that a flurry of privatisation has gripped SG market of late with the Asian consumer franchises that started the corporate actions.

Next, bombed-out cyclical coal stocks went the route of privatisation as well. Stocks have generally ended up more than 20% higher on such buyouts. House note stocks that might receive privatisation offers include Chemoil, CH Offshore, Hiap Seng, KS Energy, Mermaid Maritime, Otto Marine, STX OSV, Yangzijiang, Bukit Sembawang, Ho Bee, Pan Pacific, Singapore Land, Great Eastern, M1, Armstrong and Biosensors and recommends positioning for these stocks, if one wants to bet on privatisation gains.

Karin Tech

Karin Tech: Reported a 35.3% YoY surge in rev to HK$1,712.9m and a 22.0% jump in PATMI to HK$36.9m for 2HFY12. After adjusting for exceptional items, core net profit would instead have declined 12.1% YoY to HK$21.4m, which was below expectations.

Looking ahead, OCBC believe that Karin’s Consumer Electronics Products segment would remain as its main revenue driver given its license to sell the full range of Apple products at its retail stores. House raise FY13 revenue forecast by 6.9% but lower core net profit estimate by 7.6% on lower margin assumptions. Maintain HOLD, with a lower fair value estimate of $0.25 (previously $0.265).

Mapletree Logistics Trust

Mapletree Logistics Trust: Announced on 28 Aug that it will acquire Hyundai Logistics Centre in Gyeonggi-do, South Korea for a consideration of $24.6m. Separately, MLT entered into an agreement to divest 30 Woodlands Loop in Singapore for $15.5m.

The sale proceeds will be redeployed to partially fund the acquisition in South Korea. OCBC view both transactions positively as it clearly reflects MLT’s capability to optimize portfolio returns through proactive asset management. House tweak forecasts to accommodate the two transactions. FY13-14F DPUs are raised by 0.3-0.7%, but there is no change to our fair value of $1.19. Maintain BUY.

Guocoland

Guocoland: Great 4Q results reversing FY12 from a loss. 4Q rev at $319.7m up over 3 fold yoy with net profit at $66.1m +47.5% yoy. The higher rev was attributed to co’s residential projects in Sg and Shanghai Guoson Centre’s office blk.

Co guides that sentiment for luxury homes continue to be cautious following cooling policy measures though suburban demand remains stable. In China, govt measure also continue to slow demand.

A dividend of 5c have been proposed.

Sembcorp Ind

Sembcorp Ind: Has form a 49% owned JV with publicly listed Indonesia co Kawasan Indstri Jababeka to co-develop and urban development (industrial park) in Central Java. The JV will have US$20m in initial equity and Sembcorp Ind’s share will be approx US$9.8m which will be internally funded.

Dukang Distillers

Dukang Distillers: Reported a strong 30% yoy rise in net profit to Rmb218.09m for FY12 Turnover increased 28.1 per cent over the previous year to RMB1.83 billion, thanks to an increase in revfrom Luoyang Dukang's operations. Overall gross profit margin for Dukang brand products increased to 41.4% from 39.2% yoy, mainly from the launch of its premium Jiuzu Dukang product series.

Grp note that it will continue to place emphasis on growing brand equity and strengthen its positioning to target mid to high class and mass-market consumers respectively in Henan Province and the rest of China.

Add that according to the latest data released by National Bureau of Statistics of China, the baijiu industry achieved sales of Rmb374.7b and profits of Rmb57.2b in 2011, representing a growth rate of over 30.0% yoy. In light of the continuous expansion of the Chinese baijiu market, the Gup expects to increase its production capacity for brand products by about 40% or 3,000 tonnes through the addition of another 700 fermentation pools during FY13.

Yongnam

Yongnam: Grp has secured a significant project worth $21.3m to supply, fabricate, surface-treat and deliver 7,000 tons of structural steel for a belt conveyor structure for German co, Beumer Group in Msia.

This is Yongnam’s first significant project in Msia since its last major project at Tanjung Bin Power Plant in 2005 and grp note that the contract signals the re-opening of an old mkt which has the potential to provide a stream of new contracts as grp continue to diversify its markets. Project is expected to be completed in 3Q13 and is expected to have a positive impact on grp’s FY12 results.

We note that latest contract win brings grp’s orderbook to approximately $496m, underpinning earnings visibility till 2014-2015.

Separately, grp is also expected to be a major beneficiary in SG’s latest announcement in the construction of the $18b MRT Thomson Line announced yesterday, with backed by its very strong track record in the recent construction of SG’s Downtown Line. Grp has also in its latest qtrly presentation earmarked the Thomson Line as an upcoming potential project to bid for.

Thomson Line / Potential beneficiaries

Thomson Line / Potential beneficiaries: SG govt has announced SG’s 6th rail network ‘The Thomson Line’ (TSL) which will open from will open from 2019, instead of the indicative timeline of 2018 announced in the Land Transport Master Plan. TSL will run from Woodlands in the north to Marina Bay in the south and is expected to be built at an estimated cost of around $18b.

Analysts note that properties along the line can expect an initial 10% rise in property prices in the initial stages and further upside once its in operation, although expect impact not to be that great for prime locations nearer to the city, e.g Orchard.

We note that TSL will be fully underground, and with an estimated cost of $18b, which could leave a sizeable portion of contracts to be up for grabs by our construction companies. Potential Co’s that could gain from potential contract wins would include Yongnam, CSC, Hock Lian, TTJ, CSC, Koh Bros, Tritech and Lumchang. (Yongnam could still be recognized as the clear leader in tunnel strutting and steelworks)

Ausgroup

Ausgroup: Reported good set of 4Q12 results. Rev at A$175.3m, +18.3% yoy and -3.8% qoq, while net profit at $8.3m, +88% yoy and +22% qoq. Result brings FY12 rev to $632m, +5% yoy and net profit to $23.3m, +88.1% yoy. Gross margins increased to 12.4% vs 9.6% yoy.

Strong rev was due to grp’s integrated services segment and fabrication and manufacturing segments which recorded an increase in activity, but the major projects segment posted a fall in rev due to the timing of awards of contracts.

Grp has proposed a div of 1c/share (0.64c final and 0.36c special). Grp’s fundamentals remain strong with a net cash position of $26.7m, while orderbook stands at A$324m, underpinning earnings visibility for ½ a yr. Grp has secured A$792m contracts in FY12 and has about A$593m worth of tenders submitted to date. (Speaking to grp’s mgt, reveals that they are fairly confident that FY13 orderwins should exceed that of FY12)

Going forward, grp remains confident of prospects, noting that expressions of interests by clients are at record levels, with a number of committed projects entering construction and maintenance stages, which would lead to increased demand for integrated service providers. At current price, grp trades at just 6x P/E. (Ex-cash at 5.1x) vs Civmec’s forward annualized P/E of approx. 19x.

Other key notable factors during analyst briefing was the presence of some fund managers, which includes Lumiere Capital, a well-known local fund specializing in investing in small-mid cap co’s.

SG Market (30 Aug 12)

SG Market: S’pore shares are likely to track stalling Wall Street as investors wait out the calm before Ben Bernake’s Jackson Hole speech and the oncoming events on Sep 6 and 12. While this Fri’s gathering may be a non starter, the risks are definitely to the downside. Immediate support for the STI remains at around the 3040 level with likely resistance at the 3088 year-to-date high/

Among companies in focus, AusGroup reported a good set of 4Q results with net profit surging 88% yoy and 22% qoq to A$8.3m. Rubber-linked shares such as GMG and Goodpack may be in focus after major natural rubber producers Thailand, Indonesia and Malaysia firmed up a deal to limit rubber exports in an effort to support prices. Yongnam landed a $21.3m contract for a Malaysian project. Sembcorp Industries signed a JV deal for a new urban development in Indonesia. A study published in JAMA showed Biosensors' BioMatrix stent is more effective than a bare-metal stent in treating patients with acute myocardial infarction.

Wednesday, August 29, 2012

Marco Polo

Marco Polo: Share price at +2.9% today. Recently there has been a substantial amount of shares buy back by key co. personnels on the 17/08/2012 by Mr Lee Wang Tang 2000 Lots at 0.34c and Lai Qin Zhi 2000 Lots at 0.34c. Following on 22/08/2012 another 2000 Lots had been taken up by Mr Lee Wang Tang. These transactions carries a significant percentage of the vol traded on the particular counter and perhaps it will give the current shareholders a certain belief and confidence in the co.

Dairy Farm

Dairy Farm: CIMB analyze Carrerfour's withdrawal on Dairy Farm. Note that Carrefour’s withdrawal from SG bodes well for Dairy Farm, as not only will Dairy Farm get a chance to extend its local market leadership, but it can also swoop in on Carrefour’s retail staff, a boon in the current tight labour market.

Add that Dairy Farm has the potential to step into Carrefour’s shoes and extend its mkt leadership after Carrefour’s departure. Through its Giant banner, it holds more than 50% of the hypermarket market by number of outlets (8), outmuscling its nearest competitor, co-operative NTUC FairPrice (5 hypermarkets in the suburbs). Even before Carrefour’s decision to leave Singapore, Dairy Farm was set on opening a new Giant hypermarket at Suntec (site secured).

Now, it will be exploring options to take over Carrefour’s outlet at Plaza Singapura. House estimate Carrefour’s sales at €100m from its 2 outlets, or around 10% of Dairy Farm SG’s revenue. This is the

potential wallet share for the remaining incumbents. Further, Carrefour’s withdrawal will allow Dairy Farm to swoop in on its retail staff, a boon in the current tight labour market. CIMB Maintains O/p with TP US$12.00

Hyflux (technical)

Hyflux: Counter is testing its support at $1.35, Stochastics is approaching the oversold lvl and may bottom out while RSI has appeared to start heading up. Technicals are overall still down but are signalling a possible bottom esp since this is a support lvl. Another break will likely see counter trade to $1.26 lvl. Upside is capped by resistance at $1.45

Ezra

Ezra’s shareholders will receive 1 Triyards share for every 10 ofEzra’s. The listing of Triyards is part of Ezra’s plan to realign itsbusiness towards greater focus on its subsea and offshore division. Ezra will retain amajority control of 67% in Triyardspost distribution.

CIMB neutral on the transaction as Triyards only contributes 3-4% of Ezra’s earnings. Triyards’ order book is about US$150m-200m p.a., comprising fabrication of liftboats, self-elevating platforms and topsides

and internal shipbuilding/repair works for Ezra. Add that the listing of Triyards is unexpected but it raises the prospect of fund-raising at a later stage. There are pockets of growth opportunities, especially in Brazil where fabrication capacity is in demand. However, this may require capital injection, which Ezra may not be able to fund given its own stretched balance sheet.

The dividend in specie distribution route is the best option given the choppy equity market, speeding up the process of listing as it meets SGX's rule of having minimum 500 shareholders. Finally, the dividend in

specie of Triyards shares could be the only dividend that Ezra shareholders would receive for FY12 as there may not be further distribution from the Ezra group. House maintains O/p on Ezra with $1.38 TP.

Rowsley

A read through on Rowsley recent 1Q12 results showed that the co. was still loss making, with net loss at -$742k vs -402k yoy. The increase in the loss amount was largely attributed to the non-recurrence of div income, increase in other loss incurred and record of share of loss from the associated co’s in the reporting period.

Basically, the stock does not have much fundamentals, it only holds stakes in an associated co. Streamax, which also reported losses and continues to be adversely affected by global decline in nickel prices and production issues at its supplier’s factory.

Apart from that, the only comforting point is that the grp is in a net cash position of $6.2m, with no debt, and has $8.3m available for sale financial assets and that Peter Lim still owns abt 29.8% of the co’s shares.

UPP (technical)

UPP: Technical Buy Call by UOB Kay Hian with potential 25% return and $0.375 TP. Note that a break above $0.31 could test our target as prices have closed above its mid Bollinger band. Its Stochastics indicator has hooked up and its MACD has trended up albeit below its centerline. Tight stops could be placed at below $0.27.

Sakari

Sakari: Offer has become unconditional after the grp it reached an agreements with sellers to acquire 51.8m shares, taking its stake in the co to more than 50% from 45.4% previously. CIMB says the offer price is attractive, representing a 28% premium over Fri’s close and 9% premium over SAR’s 52-wk VWAP. House advocate accepting the offer and expect the share price to rise to $1.90 once trading resumes.

Add that the offer price is fair, translating into 15x CY12 P/E vs. the stock’s 14x historical average since its 2006 listing. The offer price is also generous vs house previous $1.00 target price (9x CY13 P/E, 1SD below its 3-year mean). Deem this an attractive exit opportunity as poor earnings prospects imply few re-rating catalysts in the medium term if not for this offer.

Biosensors/MicroPort

Biosensors/MicroPort: Biosensor’s peer Microport announced 1H12 results which was better then expected. Total rev at Rmb848.9m, +8% yoy, while net profit at Rmb2226.7m, +9.4% yoy. Rev from vascular device products rose by 3.3% yoy in 1H12, accounting for 94.7% of total rev. Of which drug eluting stents (DES) generated Rmb401.9m. TAA/AAA stent grafts brought in stable revenue stream in 1H12 compared to 1H11.

Other stents generated strong growth of 54% yoy, mainly due to the rapid growth of intracranial stent system and other new consigned products. EP device and diabetic device segments have achieved revenue of Rmb 3.6m and Rmb 5.0m in 1H12, respectively, grown rapidly by 44%yoy and 216% yoy from 1H11. Suzhou Best, acquired in Nov 2011, have started to generate earnings for the co. The orthopaedic business revenue was Rmb16.9m revenue in 1H12

Profit margin improved on decreasing production cost and R&D expenses. Gross margin improved from 84.6% in 1H11 to 85.2% in 1H12, mainly due to the declining manufacturing costs of the drug-eluting stents, benefiting from the improvement in the production technology. UOB Kay Hian maintains Buy with HK$4.70.

We note that positive results could stir some positive sentiment for SG Peer BioSensors, who operates in similar spheres.

Raffles Edu

Raffles Edu: Proposes 1 rights share for every 5 existing shares at $0.14. Co expects to raise net proceeds of $23.7m if fully subscribed and apply the proceeds for the repayment of loans, investment and working capital. Co currently has negative net working capital of $119.0m

Starhill Global REIT

Starhill Global REIT: Court of Appeal dismisses appeal by Starhill and does not find that the rent review mechanism with Toshin has been rendered inoperable. Both parties are to jointly request the Singapore Institute of Surveyors and Valuers to appoint 3 valuation firms to determine the prevailing market rental rate. Legal costs will be borne by both parties with each bearing their own costs.

The case first arose when Starhill disputed the rental review contract with its tenant Toshin which is the master lessee of Ngee Ann City. Both parties will continue in their landlord-tenant business relationship after this. This is not expected to have an overly adverse effect on Starhill esp since an earlier decision was ruled in favour of Toshin

China Minzhong

China Minzhong: CIMB downgrades to neutral from OutPerform and Cuts TP to $0.78 from $0.81. Note that 4Q12 net profit came in ahead of expectations, but house tweak estimates on housekeeping and lower TP, still pegged to the sector’s 3x P/E.

House concerned that operating cash flow at Rmb359m makes up only 52% of earnings because of the lengthening of its receivables days. Mgt believes that credit quality is good and short-term liquidity needs should be covered by its approximately Rmb600m in undrawn credit facilities.

Maybank Kim Eng however maintains Buy with $1.16 TP citing that sharp increase in receivables has improved and expect possible first div payments this yr.

Ascendas H-Trust

Ascendas H-Trust: DBSV initiates coverage on Ascendas HospitalityTrust (A-HTRUST) with a BUY recommendation and targetprice of $ 0.95. Note that as the first hospitality trust with both a REITand an active business trust structure, A-HTRUST offersinvestors a higher beta proxy to major source of consumptiongrowth in Asia – corporate and leisure travel. A-HTRUST has awell-located portfolio spanning key growth markets in the AsiaPacific.

Its collaboration with Accor Asia Pacific, a well-knowninternational hotel operator, will help to rejuvenate and propel its initial portfolio to new heights, in addition to offering apotential pipeline for growth. A-HTRUST offers an attractiveFYP13F-14F yield of close to 7.8-8.1%, 200 bps above the SREITsector.

Felda Global Ventures

Felda Global Ventures: Grp’s 1H core earnings came in below expectations at only 40% of our and 39% of consensus full-year earnings. The negative surprises came from weaker production, higher costs of production, lower sugar contributions and the RM40.6m listing expense charge. CIMB cut FY12 net profit forecast by 6% to account for higher costs, listing expenses and lower FFB production and fine-tune FY13-14 earnings by 1-2%. Maintain Neutral with a lower target price, still based on a 10% discount to SOP. See near-term support from its 5.5sen interim div and M&A possibilities.

Ascendas Hospitality Trust

Ascendas Hospitality Trust: (Flash Note): Initiated at Overweight, $0.98 TP by HSBC.

Suntec REIT/ CMT

SG Supermarket/Suntec REIT/ CMT: Initial concerns on the vacancy created by Carrefour appears to be resolved, after Dairy Farm Singapore says it has signed a lease to open a new Giant hypermarket chain at Suntec City. It is also exploring the possibility of taking over the space at Plaza Singapura after Carrefour ends its lease.

Note that Dairy Farm is the owner of Coldstorage and Giant in SG, and the second biggest supermarket operator after NTUC.

Intraco / Hanwell

Intraco / Hanwell: Tycoon Oei Hong Leong has called off talks to buy a substantial stake in Intraco after he failed to secure promises of support from the major shareholders of Hanwell Holdings. This will deprive Intraco shareholders of a potential 70c/share general offer from Mr Oei, who had initially said that he would offer to take the co private if he could acquire the Hanwell bloc.

Eu Yan Seng

Eu Yan Seng: FY12 results in line with our estimate but below consensus. Rev grew 8.9% yoy to $289.9m, 5.3% while net profit -35.2% yoy to $16.4m. Excluding exceptional items ($8.8m relating to consolidation of Australian business and S$7.1m revaluation gain on investment properties), adjusted FY12 net profit came in at $18.1m.

Retail sales performance in its core markets of SG, Msia and HK were disappointing. Sales were dampened by a weaker retail environment, as well as the relocation of existing stores due to higher rental renewals in HK. Same-store sales growth (SSSG) across all three regions was negative. (HK: -2.3%, SG: -2.6%, Msia: -3.7%).

Going forward, UOB Kay Hian that core mkts are likely to remain under siege. Expect SSSG to remain flat in the current economic environment. Operating margins will be under pressure from higher rentals, especially in SG and HK, with mgt estimating a 12-15% increase per year. Mgt does not rule out the possibility of acquiring more properties going forward to secure prime retail locations.

Ratings as follow:

UOB Kay Hian maintains Sell with $0.51 TP

Pteris Global

Pteris Global: To place 82.2m shares at $0.13 at 14.8% prem over VWAP of $0.1132 to China Intl Marine Containers (CIMC). The shares will be new shares, approx 15% of enlarged share capital. This will raise gross proceeds of $10.7m which co will use has working capital

CIMC is a conglomerate involved in the manufacturing and supply of containers, special purpose vehicles and heavy trucks,equipment for the energy, chemicals and liquid food industries and offshore engineering. It has over 150 subsidiaries and 63k staff globally.

While dilutive to shareholders (NAV down 4.42% to 17.3c, EPS down 11.1% to 0.08c) , the price paid is higher than current mkt price and the investor is also apparently a big co which might lend support through its network.

SembMarine

SembMarine: Secured a contract worth US$674m for construction of 8 modules and module integration works for 2 FPSOs from Tupi, a consortium owned by Petrobras Netherlands, BG Overseas Hldgs and Galp Energia. The projects are scheduled for completion in 60 mths and will be deployed in the Tupi field in Brazil. All the work will be done in co’s Brazil subsidiary Estaleiro Jurong Aracruz.

The contract comes with an option to construct 4 modules and modules integration for a FPSO to be exercised within 18 mths of the contract signing.

SembMarine has secured YTD orders of $9.2b

DMG maintains Buy with TP$5.70. House is of view that spending for offshore projects will remain robust given Brent and WTI crude oil prices are above oil majors’ invt hurdle rate of US$75-80 per barrel

OCBC maintains Buy with TP$6.09

Sin Heng

Sin Heng: Reported a 31% yoy rise in 4Q12 profit s to $3.77m. Rev rose 14% yoy to $38.73m mainly due to an increase in rental and trading rev. Full-year profit rose 16% yoy to $9.33m. The group has maintained its final dividend of 0.55c per share for the year.

Grp note that its complementary business model of rental and trading of cranes and aerial lifts have proven to be successful in Msia, SG and Vietnam and intends to replicate this business model in other mkts. Add that its recent JV in Myanmar remains on track and is always on constant lookout to explore on possible business opportunities in the region.

IHH Healthcare

IHH Healthcare: Announced strong set of 2Q12 results, which was in-line. Earnings rose more than five-fold to RM403.54m ($162.1m) yoy. Rev at RM2.7b, +231% yoy. Strong results due to the recognition of profits from the sale of 216 medical suites at Mount Elizabeth Novena Specialist Centre, and the consolidation of Acidadem Holdings from Jan12. Normalised revenue, which excludes the sale of the medical suites, was RM1.5b, +82% yoy.

Deutsche note that growth in inpatient admissions and revenue intensity due to price increases and case mix helped lift 1H12 EBITDA margin by 1.1ppt yoy to 21%. The outlook remains positive as mgmt accelerates the ramp up of Novena going into 2H12.

Ratings as follow:

Deutsche maintains Buy with Rm3.55 TP

Olam

Olam: Announced 4Q12 results which were in-line but at the upper end of estimates. Rev at $5.15b, +12.7% yoy and +21.7% qoq, while net profit at $109.5m, -14% yoy and +10.9% qoq. Result brings FY12 rev to $17.1b, +8.2% yoy and core net profit to $355.5m, -4.6% yoy. NC margins for the qtr at 8.5% vs 8.9% yoy and 7.9% qoq, while NC margins for FY12 at 8.1% vs 7.7% yoy.

Total Sales vol for the qtr at 3.5m mt, +50.7% yoy and +29.6% qoq, led by grp’s food related business segments, which accounted for 76.4% of grp’s rev and 87% of NC. Grps performance was however dragged by lower NC’s from its non-food categories consisting of IRM and Commodity financial services, due to unfavourable and volatile conditions, esp in Cotton. (See segment preview below for more info on the diff segments) Grp’s bottom-line was also attributed to a sharp rise in other operating expenses at $174.6m, +109% yoy and employee benefit expenses at 180.1m, +81.9% yoy.

Going forward, grp note that the cyclical events experienced over the past year in the IRM and CFS segments could have some continuing impact in FY2013. However, Olam remains positive about the long-term fundamentals of the industry, as well as the overall business model and will continue to execute on the strategy to grow long term intrinsic value across all existing business segments.

Ratings as follow:

CIMB maintains O/P with

Deutsche maintains Buy but cuts TP to $2.30 from $2.90

UOB Kay Hian maintains Buy with $2.55 TP

OCBC maintains Hold with $1.60 TP

Maybank-KE maintains Sell with $1.75 TP

Segments preview as follow:

1) Edible Nuts, Spices & Beans: Edible Nuts and the Spices & Vegetable Ingredients businesses performed well, supported by increases in almond production from Australia and US, above plan performance of US and Argentinean Peanut operations, introduction of Hazelnuts into the portfolio (with acquisition of Progida Group) and expansion of spices business with acquisition of Vallabhdas Kanji in India.

2) Confectionery & Beverage Ingredients segment: Continued to register strong NC growth. Cocoa business had another good yr, despite very lacklustre market conditions. The integration of Macao Commodities (Spain) and Britannia Foods (UK) provided additional sources of value and increased Olam’s presence and reach. Coffee business performed well with mkt share gains in most origins, including new Arabica operations in Mexico and Guatemala.

3) Food Staples & Packaged Foods segment: Recorded stong sales Volume and NC growth at 84.5% and 34.7% respectively. Rapidly expanding Grains business drove strong vol and NC growth. Dairy and Sugar businesses faced difficult market conditions due to unfavourable trading and adverse weather conditions. The Packaged Foods business gained further momentum with several acquisitions during the year contributing to the expansion of Olam’s product offering and distribution reach in West Africa.

4) Industrial Raw Materials segment: Dragged on grp’s NC, with vo l, +7.5% and NC -48.0%. Margin per ton was reduced by 51.6% to S$135. Cotton business, particularly the Australian, Brazilian and the US origination and marketing operations, was impacted by extreme market volatility, declining volumes from growers and enhanced customer counterparty risk in some Asian markets.

SG Market (29 Aug 12)

SG Market: S’pore shares may remain stuck in neutral amid a lack of strong cues from Wall Street and ahead of Friday's big show by the Fed. Traders are waiting for clues in the lead-up to the Jackson Hole meeting but are none the wiser which path Bernanke will decide to take. The STI remains range-bound with 3030-3040 support zone closely watched, while resistance at the 3088 year-to-date high is unlikely to be troubled.

Among stocks likely in focus, Olam reported 4Q12 results which were at upped end of estimates, while IMM 1H12 results were in line with estimates. SembMarine’s Brazilian unit landed a US$674m Petrobras-related contract to build modules for 2 FPSOs.

Viz Branz (technical)

Viz Branz: Technicals look bullish after counter reversed from oversold levels on a Marubozu. Stochastics is now higher after a positive divergence and still looks to head higher. MACD is recovering from a bottom and will enter positive territory soon. RSI is also pointing up above the 50 mark. Counter will likely test resistance at $0.74-0.75 lvls within the nxt few days. Support at $0.64 region.

Longer-term trend is still bullish.

Friday, August 24, 2012

Kreuz

Kreuz: DBS Vickers believes valuations are unjustifiably cheap, noting 2Q12 net profit of US$13.3m, +29% qoq, was above expectations on accelerated revenue recognition, while 1H12 net profit of US$23.6m was nearly 75% of its FY12 estimate. It expects margins to improve with the 2Q12 acquisition of a diving-support vessel as it eliminates the higher costs of hiring third-party vessels.

Year-to-date order wins of US$155m surpassed DBSV's US$150m full year forecast and it does not rule out further upside. It expects FY13 order wins to be similar given the region's robust offshore E&P activity.

House sees 2H12 earnings to decline on seasonality factors but still forecasts FY12 net profit growth of 16% and raises FY13 earnings estimate by 5% on potentially better margins, translating to FY11-13 net profit CAGR of 18%. Despite a healthy earnings outlook, the counter has underperformed the market and is still trading below 4x FY13 P/E. It keeps its Buy call with a $0.43 target.

Genting SP

Genting SP: May give back some of Thursday's 3.7% climb to end at $1.385. The gains came amid a lack of news. It has been one of the more sold down stocks and we're probably seeing people using the high-beta to play the market, says OCBC. Its 10-day moving average around $1.32 may offer support.

City Dev

City Dev, Stochastics appears to be coming out from Oversold territory, although RSI appears somewhat neutral. Counter is currently trading between its 20 and 50 day EMA, acting as the support and resistance respectively. A break of either the support/resistance could reenforce the new trend.

Ausgrp

Ausgrp: RBA governor Glenn Stevens stated that he was optimistic on Australia's economy and refuted the resource minister's comments that Aus mining boom was over. Stevens was of the view that the peak in resource invt shld occur within the nxt yr or two. This might lend some support to Ausgrp's and by right even Civmec's share price.

On a co-specific angle, Ausgrp has underperformed Civmec recently (although still rising) and investors might also be making a bet on its results out on nxt Wed, 29th Aug aft mkt.

Sembcorp Marine

Sembcorp Marine: Citi maintains Buy with TP$6.10 on discussion with mgmt. Recent drillship win with Sete Brasil shows shift in co’s capabilities from jack-ups/semi-subs to drillships. SembMarine also believes its new yard in Espirito Santo is ideally located and will be able to obtain maintenance and repair contracts near the oil-rich Tupi yields. Demand is expected to remain firm across jack-ups, semi-subs and drillships with rigs prices to appreciate slightly resulting in higher margins. Its new yard in Sg will also be fully operational by 2013 and add $500-600m rev of high-margin repair work.

Biosensors

Biosensors: Religare initiates coverage with a BUY rating and $1.48 TP. Note that the co has emerged as a leading competitor in the US$6b global market for drug-eluding stents and expect it to continue gaining share by virtue of its innovative technology and strong position in Asia.

Tip grp to Biosensors to continue gaining share in the drug-eluding stent (DES) market: with the co emerging as the industry's #4 player by virtue of technology advantages that address DES' clinical shortcomings. In addition, Biosensors' focus on faster-growing Asia Pacific markets (including China) should drive growth above the industry's 3-4% growth globally.

DBS

DBS: Moody's confirmed all of DBS' ratings and assigned a negative outlook, citing its regional ambitions and its rapid growth in the USD trade finance business amid tighter funding liquidity. Highlights potential financial impact of Bank Danamon acquisition on DBS' creditworthiness was manageable when taken in isolation, but ‘proposed transaction provides further evidence of the grp's expansion ambitions and changing credit profile due to its rapid growth in size and geographic scope in recent yrs, a trend that underpinsnegative outlook.’

Add its ratings are unlikely to move up given the assigned negative outlook, and ratings could be downgraded if overall risk profile increased significantly as a result of aggressive expansion into higher-risk mkts or sizeable acquisitions without sufficient funding to maintain its strong capital ratios, or a non-performing ratio rose >2%.

Far East H-Trust (IPO)

Far East H-Trust: Far East Hospitality Trust saw its public offer of 50m stapled securities approximately 14.6x subscribed by retail investors. The total demand of approximately 8.77b stapled securities under the placement tranche and the public offer represents approximately 27.6x over subscribed.

The Trust secured 10 cornerstone investors, including Aberdeen Asset Mgmt Asia, AIA Grp, NTUC Income Co-operative. Trading expected to commence at 2pm on 27 Aug. Indicative grey market price for the IPO is rumored to be at ard $0.97-$0.98.

Frencken / Juken

Frencken: Voluntary conditional offer for Juken shares has firmed up. Co will offer $0.18 per share or 1 new Frencken share for every 1.8 Juken shares held. The was made after sh/h approval at EGM yday.

PEC

PEC: Good quarter results. 4Q Rev at $140.7m +38.8% yoy +31.9% qoq with net profit at $4.5m +29.7% yoy 5 fold qoq. Co is seeing a decrease in gross profit due to cost pressures and pricing competition. Co expects FY2013 to remain challenging given the environment but has a healthy orderbook of $258m as of June-end 2012.

Div of 2.5c declared.

Cordlife

Cordlife: Reported a 12.1% increase in rev to $28.8m, although net profit declined 18.3% to $6.9m due to one-off ipo expenses. Without IPO expenses, net profit up 4.1% to S$8.8 million Rev driven by rise in number of client deliveries and new cord tissue banking services in Hong Kong, while group achieved higher gross margin of approximately 70.0%. Overall fundamentals remains strong with grp in a net cash position.

Grp has declared dividends of 3.8c to date and remains poised for further geographical expansion with recent proposed acquisition of China’s largest cord blood banking operator.

Oxley

Oxley: Reported a 73% YOY decline in net profit to $1.67m for 4Q12 even as turnover rose 16%. Full-year profit rose 26% yoy to $16.9m mainly driven by rev recognition from the sale of 11 of the group's residential projects which have commenced construction, including Parc Somme, which obtained its TOP in May 2012. Profit was also partly boosted by rental income from the corporate office at Robinson Road, where most lease obligations were in place prior to its being acquired in February 2011.

A final dividend of 0.47c per share has been proposed. Together with the interim dividend of 0.1c, the total dividend per ordinary share for FY2012 will be 0.57c.

SG Market (24 Aug 12)

SG Market: S’pore shares are likely to face losing interest following the tumble on Wall Street on global economic worries as well as fading hopes of quick stimulus action by the Fed. The technical landscape is also showing signs of tiredness with momentum indicators easing off. Support for the STI is likely to be found around the 3040-3050 range, followed by the psychological 3000 level.

Not much market moving news today. Among stocks likely in focus, Oxley posted disappointing 4Q results with net profit -73% even as revenue rose 16%, while PEC reported 30% rise in 4Q profit. . Tiong Woon posted a FY12 loss of $5.8m despite revenue rising 41%. Myanmar oil play Interra's proposed rights issue was approved at an EGM. Far East HTrust public offer was 14.6x oversubscribed by retail investors. Grey market price touted at $0.97 vs $0.93 IPO price.

Thursday, August 23, 2012

Raffles Edu (technical)

Raffles Edu: Counter appears to have bottomed out and is turning positive in the near-term. Stochastics and RSI are up from oversold levels, MACD is also moving into positive territory. Resistance seen at $0.39-0.395 lvls Prev recent low at $0.355 serves as support lvl.

Longer-term trend is still negative however with 50 day SMA still below 200 day SMA.

Raffles Edu has guided for a loss for FY2012 results expected on or abt 24 Aug 2012.

Sakari

Sakari Resources: UOB KayHian tips the stock chart as a technical at Buy with $1.70 target. Highlights the stock appears to be staging a strong rebound at its mid Bollinger band or near $1.40, a level to hold for further upside. Notes its 20-day moving average looks poised to cross above its 50-day moving average and a break above $1.57 is likely to result in this target being achieved. It recommends watching for possible bullish crossovers on its MACD and stochastics indicators. Stops could be placed below $1.39. The stock is up 1.7% to $1.505 on solid volume.

Olam

Olam: DBS Vickers reckons Olam is not out of the woods yet. House expects 4QFY12 core earnings to rise 12% qoq to ~$90m on its almond harvest and coffee origination, but the industrial raw-materials segment should offset other segments' gains, with its net contribution possibly dropping 71% yoy on lower cotton and timber volumes.

Highlights there is potentially further downside risk to 4Q12 expectations from weaker than expected US/European dehydrates/cocoa/chocolate/cotton demand. Adds, it may take longer for Olam's free-cash-flow to turn positive. While it likes Olam's growth prospects and strong management team, the group has been in negative free cash flow, given its heavy investments over the last 5 years amid skittish market conditions. It now expects positive FCF next year, but much will depend on the level of capex outlay needed for potential M&As. DBS keeps its Hold rating with $2.00 target.

OSIM

OSIM: DMG maintains Buy with $1.75 TP. House We recently hosted OSIM for a roadshow to Malaysia. Note that their product pipeline is set for next year and we should expect two new chairs, which should drive earnings momentum in FY13/14.

Some investors were concerned over the impact of a slowdown in China but management appears confident impact will be minimal as chair penetration rates there are still very low at 1%. In terms of combating copycats in China, OSIM stands out by targeting the premium end of the segment which value quality, durability and after-sales service.

House have also been busy scouting out the showrooms of OSIM, Ogawa and Otto and found that OSIM offers the most extensive range of products among its peers in terms of price points as well as choices of colours. Finally note that mgt has its heart still set on getting 55%-owned Brookstone re-listed in the US by 2014, which could be a kicker to earnings.

Moya Asia

Moya Asia: Sias Research note that grp maintained its healthy performance for 1H12 with revenue and PAT coming in at $19.7m and $1.6m respectively. Early last month, co. announced the disposal of stakes in some China assets and will free up about RMB15m cash (subject to approval at EGM). The proceeds, together with the invested capital from the nearing completed Cambodia project, will probably be channeled into their secured BOT projects in Indonesia.

Bekasi phase one is expected to be completed in 4Q FY12 and house expect passive income to start flowing to Moya Asia thereafter. That said, Bekasi phase two and Tangerang phase one will probably commence work soon and generate construction revenue for the company. Overall, maintain Increase Exposure with an adjusted intrinsic value of $0.170.

Wilmar

Wilmar: Citi hosted management for an investors’ event post 2Q12 results. House see a change in message from the company as mgt shared that it will be more risk averse in the future (i.e. less taking of trading views), which implies reduced earnings volatility in the future. Wilmar’s equity valuation has been severely impacted by earnings volatility from its oilseeds division, which investors have partly attributed to trading views.

Note that seasonal strength expected in 2H12 should allow for better financial results and likely mark 2Q12 as Wilmar’s worst qtr. Following stock price weakness, its valuation is at near GFC trough with investors seeing it more as an industrial firm. Equity valuation for Wilmar will likely recover more significantly to reflect more normalized earnings power post two quarters of expected better results and investors being able to better gauge its ability to use scale and logistical advantages to consolidate an overbuilt Chinese oilseeds crushing industry.

House maintains Buy with TP $4.08.

Tat Hong

Tat Hong: CIMB maintains OutPerform with TP $1.39. House note that robust margins, rental rates and utilisation for its crawler and mobile-crane fleets should persist in the next few years, given a wealth of regional projects. In recent road show, Mr Roland Ng, grp’s MD, expressed unbridled confidence that the higher margins, rental rates and utilisation could be sustained. Catalysts expected from further sets of strong results and efforts to reward shareholders through dividends.

IHH Healthcare

IHH Healthcare: Deutsche initiates Coverage on stock with Buy Call and TP RM3.55. Note that IHH ranks among the largest private healthcare companies globally. Positioned in the higher-growth healthcare markets of Asia and CEEMENA, strong capacity expansion should drive robust two-year (FY12-14E) adjusted EBITDA growth of 26%.

Mgt’s expertise, branding and balance sheet capacity should also give IHH an edge in pursuing new opportunities. TP implies 19x FY13E adjusted EV/EBITDA, or a 26% premium to its Asian healthcare peer average of 15.1x. Believe the valuation premium is justified as IHH is 4-5x the size of the market leaders in Thailand and India and has a larger footprint and a stronger forecast growth. Believe that IHH should also trade at a premium to Parkway Holdings’ historical 17x EV/EBITDA from 2006-10.

Hanwell/Intraco

Hanwell/Intraco: Hanwell has accepted tycoon Oei Hong Leong's $20.6m offer for its stake in Intraco and is working towards finalising the sale-and-purchase agreement. This came a day after Mr Oei set a deadline for the deal, saying he will withdraw his 70 cent-a-share offer if an agreement was not inked by 5pm next Tue. Transaction will be conditional upon approval from Hanwell's shareholders at an egm (if required), and has to be completed by no later than 5pm on Oct17.

Hanwell is Intraco's controlling shareholder with a stake of 29.89%. Both parties are negotiating and finalising the sale-and-purchase agreement. Hanwell's latest move may mark the beginning of the end of a bidding war for its Intraco stake. Mr Oei's latest offer is the highest on the table, and he has said he will make a general offer for the remaining Intraco shares he does not own, if the deal with Hanwell goes through.

HLN

HLN: Lifts trading halt. Proposes to dispose its stake in Tianjin Swan Lake Real Estate Dev for total of Rmb74.6m. This comprises co's 50.5% sh/h interest in a JV which holds a 30% stake in Tianjin Swan and a pro-rated profit guarantee. Co intends to use the proceeds for bigger property projects.

Saizen REIT

Saizen REIT: Results reflecting turnaround with DPU of 0.63c for 2H compared to 0.50c prev yr and 0.6 last half. 4Q rev was approx JPY907.7m -0.1% yoy though net profit was up at JPY478.0m reversing a loss of JPY1.6b last yr due to JPY1.5b in fair value losses. NPI was up 7.5% qoq which property operating expenses down 4.5% qoq.

Avg occupancy rates was 91.4% compared to 90.9% but rental reversion of new contracts were lower by 2.1% overall in FY2012.

Co currently trades at 0.5x P/B with 12-mth yield of 7.8%

Book closure for div will be on the 31 Aug and is payable on the 18 Sep 2012.

Nam Cheong

Nam Cheong: (Possible positive sentiments) Grp announced that it has secured 3 contracts worth a total of US$43.81m ($54.8m).

The first vessel is a 3,000 dwt PSV for a new customer in West Africa, while the second is a 5,150 BHP AHTS vessel for a Norway-based customer and the third vessel, also a 5,150 brake AHTS vessel, is for a marine operator with an expanding fleet of offshore support vessels in MENA.

Latest contract wins bring Nam Cheong's order book to RM912m, underpinning earnings visibility till 2014 and are expected to contribute positively to the group's earnings for FY12-13.

SG Market (23 Aug 12)

SG Market: S’pore stocks are likely to drift down in the absence of clear leads from a mixed Wall Street close and as investors wait for further direction from Ben Bernanke’s much awaited speech next week, followed by the FOMC’s policy meeting in Sep. Momentum indicators for the S’pore market are deteriorating with the STI index breaching its 20-day moving average on the downside. China's August HSBC flash manufacturing PMI, due later, is likely to be keenly watched, but expectations for improvement may be priced in. The next support level for the STI lies at 3030, followed by 2985, while firm resistance appears at 3100.

Trading opportunities are limited. Among stocks in focus, casino regulators fined Genting Singapore $140,000 for casino-entry rule violations, while Nam Cheong landed US$43.8m contract wins for 3 vessels.

Wednesday, August 22, 2012

F&N/APB

F&N/APB: Heineken's move to boost its stake in APB via market trades and by buying Temasek's 1.4% stake likely makes its move to buy F&N's APB holding a done deal, an analyst says. While ThaiBev is at a loss for its F&N buys, Kindest Place will still walk away with around $170m in profits. While buying Temasek's stake appears quite small compared with what Heineken is shelling out to take control of APB, it was likely a strategic move to cover all its bases, including the possibility of taking the Tiger beermaker private. Had Kindest Place bought Temasek's 1.4% stake, the Thai company would have had around 10% control of APB, potentially complicating Heineken's plans to delist APB. What is now up for grabs is a 7.16% stake held by several minority investors. APB is flat at $53.00, matching Heineken's bid price, in strong vol after several large trades. F&N is down 1.1% at $8.26 and ThaiBev is down 1.5%, or a half-cent, at $0.335.

HPH Trust

HPH Trust: Counter is in downward slide with indicators still yet to signal a bottom. Stochastics, though in oversold conditions, are still pointing down, similar to RSI. MACD has shown a positive bar which might be the start of a bounce. The positive divergences spotted in the indicators also suggest a imminent bounce. Expect a bounce over the nxt few days, but a more solid retracement will require further confirmation.

See support at $0.70 lvls with near-term resistance at $0.75

Wilmar

Wilmar: Macquarie note that reaction to 2Q results was not as exaggerated as 3 mths ago when Wilmar announced a 34% YoY drop in its 1Q12 net profit. The stock dived 15.5% in the following 5 trading sessions.

Looking at the bright side, mgt continued to reassure that co's long term prospects remain intact and Wilmar is well-positioned to capture demand growth in Asia and emerging markets. However, it is noted that times could be tough in the near future, particularly due to the excess oilseeds crushing capacity in China.

Early this year, the shareholders of Wilmar authorised a share buy back program at its AGM. Under the plan, the company could repurchase up to 10% of its share capital. Till now, the management has not started its buy back program. Its commencement could be supportive to Wilmar’s share price as seen through the effects of Olam’s share repurchase program. or worse has yet to come?

Oilseeds & Grains division was the main disappointment in 2Q12, posting a US$40m loss. Its traditionally stronger Palm & Laurics division (CPO refining) fell short of expectation as well. The management said that crush margin was poor and was exacerbated by losses from the depreciation of RMB against USD.

House cut its medium term estimates by about a qtr, with TP at $3.00 from $4.57 (implied 2013 target PE of 11.7x). Reasons leading to the decision include 1) limited scope for upside to earnings and, 2) a return to historical mid-teens P/E multiples looks hard to justify today. Stay Neutral, but expect Wilmar to underperform from a country perspective (10% upside to their FSSTI target).

IHH Healthcare

IHH Healthcare: Credit Suisse initiates coverage with an OUTPERFORM rating and a target price of RM3.75, with 20% potential upside. Believes that IHH is one of the best-leveraged plays into EMs’ private healthcare demand growth, given the scale of its ops, the strong reputation of its clinical programmes, and its fast expanding hospitals and healthcare portfolio.

Old Chang Kee

Old Chang Kee: Has exercised an option to purchase a property at Woodlands Terrace for cash consideration of $4.2m. The Property is an intermediate terrace factory leased by JTC Corp to the vendor initially for 60 yrs from 1 Sept 1994 with land area of 1.3k sqm. It will be used for food processing and storage. The purchase will increase grp's food production facilities and co is of view that this is essential to co's overseas and local expansion plans.

Singtel

Singtel: Yday’s strength might have been due to Bharti Airtel exploring to list its tower business Bharti Infratel to raise funds which would be the largest after Coal India’s listing in Feb 2010. However, this is not the first time that Bharti Infratel is looking at an IPO and prev plans were called off due to other partners suggesting different plans. The proposed issue is expected to issue 10% of capital valued at US$8-9b.

ARA

ARA: Raised approx US$941m for its private real estate funds, ARA China Invt Partners and ARA Asia Dragon Fund II. Co is also supposedly planning a yuan-denominated IPO which would include some of its Chinese property assets in office and retail. The IPO could raise up to $800m and is set for an Oct launch. ARA currently has a P/E of 15.5x

Hu An Cable

Hu An Cable: Recently won Rmb105.6m worth of contracts from one of China’s top five power generation companies, China Power Invt Corp. The contracts are to deliver various power cables to 25 wind, solar and hydro power plants across China. An est 80% of the contract value is expected to be delivered in FY2012 with the balance in FY2013.

Hu An also trades at depressed valuations similar to other S-chips, currently at 3.4x trailing P/E

Boustead

Boustead: Co's energy div has secured a $39m contract from one of the world's largest EPC and maintenance ops. The contract involves installing key process heater systems at a large-scale new invt plant in US. Co's order backlog is currently at $343m

Cosco Corp

Cosco Corp: 51% owned subsi has secured a US$20m contract to build a jack-up barge for BAM Intl and Clough Projects. The barge will have capacity of 300 tons deck crane and operate in water depth of up to 30m, and is schedule for delivery in 11 mths time.

Lian Beng

Lian Beng: 50% owned JV has secured a contract worth approx $169.0m from Luxury green Dev for proposed residential dev at Upper Thomson Rd. The works to be executed are for 9 blks of 20 storey residential flats and 22 two-storey strata landed houses with facilities. Works are expected to commence in Aug 2012 and are due to be completed by Feb 2015. The construction co and developer is currently trading at P/B of 1.0x

Keppel

Keppel: Has finalised a contract to build a harsh env accommodation semisub worth US$315m for Floatel which follows the LOI signed earlier in Mar. This will be Floatel's 4th accom semisub with Keppel. It will meet the most stringent rules and regs for worldwide ops including the Norwegian Sector. The contract puts Keppel’s YTD wins at US$8.8b on track to beat over US$10b wins in contract previous yr. Co trades at 11.4x fwd P/E currently.

F&N/APB

F&N/APB: Temasek has sold its 1.4% stake in APB to Heineken. The shares were sold at $53 apiece in a married deal, according to Reuters and Bloomberg. Heineken is believed to have mopped up more APB shares from a hedge fund. Some 6.92m shares of APB or about 2.7% of APB's share capital - were transacted at $53 on Tuesday, including the married deal.

FJ Benjamin

FJ Benjamin: FY12 missed estimates. Full-year results came below expectations, with sales of $393.2m, and net profit of $13.5m, making up 85% of Kim Eng estimates. The group offered a final dividend of 1c, as opposed to 2cts as of FY11; this is attributed to aggressive expansion and necessary increases in working capital. House lower estimates for FY13-15 by 14-17% to account for higher operating expenses. Downgrade the stock to a HOLD on the basis of lower than expected margins and expensive valuations.

Wing Tai

Wing Tai: Core earnings in line. Rev at $202.2m, +88% yoy and +58% qoq, while core net profit at $50.3m, +41% yoy and +19% qoq. Total dividend surprised slightly on the upside, comprising 3c/share ordinary and 4c special, for a yield of 5%.

Property development contributed 53% of Group EBIT, comprising a mix of income from completed properties such as units at Helios Residences, and properties under development at Foresque Residences and L’VIV. Mgt maintained that downside risks remain particularly in the mass market segment, which explains the Group’s lack of participation in the Govt Land Sales program.

Mgt announced plans to redevelop its industrial properties at 105 and 107 Tampines Road into a 337-unit freehold condo with GFA of 297,232 sqft. Deutsche estimate breakeven cost to be $870 psf, and assuming an ASP of $1,350 psf, the development could return a healthy pre-tax margin of 36%. Estimate an RNAV accretion of 12 cts/sh.

Even as the market remains challenging, Deutsche like Wing Tai’s proactiveness in trying to unlock shareholders’ value. Reckon that Grp can maintain total dividends of 7c/share for the next few yrs, implying an attractive yield of 4.9%.

Ratings as follow:

CIMB maintains Outperform with $1.68 TP

Deutsche upgrades to BUY $1.75 TP.

Uob Kay Hian maintains Buy with $1.75 TP

Civmec

Civmec: Results generally good. 4Q rev was $113.6m +347.2% yoy with net profit at $8.4m +132.8% yoy. Higher rev was attributed to higher activity in both Oil & Gas and Mining and Other segments. Operations of the Henderson facility for the FY also allowed activities to be ramped up. Current orderbook amounts to approx $264m.

A dividend of 0.6c has been declared. FY12 EPS of 6.05c which translates to a P/E of approx 20.2x

SG Market (22 Aug 12)

SG Market: S’pore shares appear to be in a holding pattern with some downward bias pending fresh cues from Wall Street or Europe. Investors may slice some profit off and reduce risk exposure before the Fed and ECB meetings end Aug. The STI seems stuck in a rut, repeating bouncing off the 3050 level but failing to punch above 3080.

Among stocks in focus, Keppel Corp may not react too much after signing a US$315m contract to build a accommodation semi-submersible for repeat customer Floatel Int’l as this merely a letter-of-intent announced in Mar. Wing Tai posted a 16% drop in 4Q profit to $140.5m, which still beat expectations but management foresees a growing possibility of a correction in S’pore property market. Civmec 4Q net profit came in at $8.4m vs $3.6m a year ago as revenue surged to $113.6m vs $25.4m yoy on strong demand in Western Australia's O&G sector. ARA Asset plans to carve out some of its Chinese property assets to raise up to US$640m Iin a Rmb PO by end-Oct. Temasek sold its 1.4% APB stake to Heineken.

Tuesday, August 21, 2012

Europe

Europe: The German Banking Assn, which represents Deutsche Bank and Commerzbank, wants the ECB to have the sole responsibility for

regulatory supervision in the euro area. EU leaders agreed on Jun 29 to give new banking supervision powers to the ECB as part of a commitment to a banking union and called on the European Commission to outline the changes by Sep.

It is unclear how much authority the ECB will get. One option would allow the ECB to take major oversight decisions for all banks, while another would be to give it a core set of central powers to oversee all banks while delegating some tasks to individual countries.

The German proposal would mean that Bundesbank would be subordinated to the ECB, serving as country representative of the central bank.

SingTel

SingTel rebounds 2.7% to $3.38 on strong volume after a number of large trades. UOB KayHian notes that while there is no company specific news, the stock's correction recently has been fairly steep with the stock is still down more than 5% month-to-date. House also highlights that on a regional basis, there were other large-cap telcos that have done well as well due to overall bullishness on the sector as stable dividend yields have become more important. Adds there is a lot of gravitation towards the larger-cap telco stocks lately and SingTel’s recent pullback, triggered by the Moody's downgrade and some disappointment over its earnings, makes it a bit more attractive than a few weeks ago. The stock's Jul 31 intraday peak of $3.61 may offer a near-term cap.

NOL

NOL: Non-material news, co appointed a former PWC partner to the board's audit and risk mgmt committee. As a whole, the shipping and shipbuilding sector is in the red today. JES -1.3%, YZJ -1.9%. NOL is still trying to stem losses as from their recent 2Q results.

NOL: Macquarie downgrades to Underperform from Neutral, citing more downside risks to freight rates, and the market placing too much faith in carriers' ability to hold down supply as cracks are appearing on supply discipline. House notes 2013 supply growth is expected to accelerate, with the high portion of large container ships for 2013 delivery a concern as they are headed primarily for the Asia-Europe route, where demand is weakening.

It now expects a 2012 loss of US$226m from a US$34m profit previously and lowers its 2013 net profit forecast to US$55m from US$88m but raises its 2014 net profit forecast by 58% to US$328m as new vessels will lower the cost base. Macquarie cuts its target to $0.95, based on 0.8x FY12 P/B, from $1.08. However, it reckons investors should revisit NOL in 2H13 if there are evidence of NOL's success in cutting costs and on an improved supply-demand balance in 2014.

LionGold

LionGold: Signs Memo of Agreement with ASX-listed Gold Anomaly (GOA) that sees co investing A$8.5m into GOA to develop gold mining assets in Papua New Guinea. Co will invest into a convertible bond for A$2.0m at 20% premium to VWAP. The bond will have tenure of 2 yrs with coupon of 9% secured against assets of GOA. 2 Other convertible bonds will also be issued to LionGold of approx A$6.5m issued by GOA's subsidiary which is convertible for a total of 60% of the subsi's shares.

Chip Eng Seng

Chip Eng Seng: Awarded $137.7m HDB contract for building works at Bukit Panjang. The contract is for construction of 7 blks of residential buildings with 862 dwelling units and other community facilities with construction period at approx 33 mths.

As of June-end 2012, co’s outstanding orderbook was approx $364m. Currently trades at P/B of 0.7x

CAO

CAO: Terminates proposed JV for oil storage terminal at Tanjung Langsat, Johore. Co was initially supposed to invest for 26% in the JV for the construction and operation of an oil storage terminal but the time required for both the concession area and lease was longer than expected. Hence, both JV partners have agreed to discontinue their JV.

F&N

F&N: Has agreed to accept offer by Heineken to acquire interest in APB at $53 per share. The 32.4% stake is valued at approx $4.43b with its 7.3% direct stake at $994m, a 6.0% increase over Heineken's prev offer. There is also a break fee of $55.9m payable to Heineken if co’s sh/h does not approve the transaction.

Heineken will undertake not to manufacture or distribute soft drinks in Sg, Papua New Guinea, Cambodia and Vietnam if the transaction goes through and likewise F&N will not sell brewery products in these locations as well.

Heineken’s prev offer was also only for co’s direct stake while the current revised offer includes co’s entire interest. The deal is given a timeline of 120 days from 18 Aug before it lapses. This is approx 35.1x P/E and $2 lower than Kindest’s partial offer (only for direct 7.3% stake) at $55.

Cimb maintains outperform but decreases TP to $9.85 from $10.00

SG Market (21 Aug 12)

SG Market: S’pore shares are likely to drift down in the absence of overseas leads and market-moving corporate news following the end of the earnings results season. The STI appears overextended with Stochastics and MACD indicators losing momentum. Support for the index is tipped at 3040, as represented by the 20-day moving average, while resistance is capped at 3100.

Among stocks in focus, F&N and APB may rise on resuming trade at the market open after Heineken raised its bid for F&N's entire APB holding to $53/share, countering Kindest Place's $55/share bid for part of APB. Tiong SEng secures a $137m contract to build a building extension at SIM, while Chip Eng Seng won a $138m HDB contract to build 7 blocks of flats in Bukit Panjang.

Friday, August 17, 2012

F&N/APB

F&N/APB: Heineken is reportedly in talks with F&N about an increased offer for Asia Pacific Breweries, perhaps at $55 or better to all shareholders instead of Kindest Place’s $55 offer only for F&N’s 7.3% direct stake in the brewer.

F&N and Heineken share a 50-50 JV that owns 64.8% of APB. F&N also has a 7.3% direct stake in APB and Heineken 9.5%. Earlier this month, the board of F&N recommended its shareholders accept Heineken's $50 offer for the whole of APB. But a revised higher offer from Thai-based Kindest Place has complicated the deal.

The latest move by Heineken is aimed at securing F&N's support against rival offers for APB, the maker of Tiger beer. By taking full control of APB, Heineken will have a greater share of one of Asia's most profitable beer makers at a time when it is facing lacklustre sales in its home base in Europe. APB's Tiger and Bintang beer brands have nearly 50% of the beer market in Indonesia, Malaysia and S’pore. APB has 30 breweries and 40 brands spanning 14 Asian countries. It also brews Heineken beer for some markets in the region.

Even if F&N's board accepts an increased offer by Heineken, shareholders will still have to vote on the deal. That means Heineken will have to win over Thai Beverage, the largest shareholder in F&N with a 26.4% stake, and Japan's Kirin Holdings, which has 15%, in buying out APB. Both ThaiBev, which sells Chang beer, Thailand's top beer, and Kirin compete with Heineken in the SE Asian region.

STI midday review

STI: +0.1% at 3064.73 as players digest the nearly completed earnings season. Trading activities may remain thin ahead of (the) weekend as well as holidays in parts of Asia next Monday, says UOB. Expects market sentiment to stay positive for the session as Singapore's NODX came in better than it expected and as Germany's Merkel said her country remains committed to keeping the euro. Volume is skewed toward lower liners at 1.01b shares valued at only $454.5m, suggesting retail, rather than institutional interest, is dominating trade; gainers top losers 1.3 to one. The index is likely to remain in a 3050-3088 range. Defensive duo SingTel and StarHub retrace some of Thursday's losses, rising 0.3% each. IT-services provider M Development is the top-volume play, with nearly 20% of shares traded after it said it would convert its convertible notes; Value Capital Asset Management increased its stake to 14.06% from 8.45% by converting notes; the stock is up 57.1% at $0.011.

Sin Heng

Sin Heng: Grp has announced the reduction of its shareholding interest in associate co., Songcheong Engineering. As a result of the sale of the shares in Songcheon by Kim and Sin Heng, both Kim and grp will reduce each of their shareholding in Songcheon from 0.5m shares (50% of the shareholding interest in Songcheon) to 0.2m shares (20% of the shareholding interest in Songcheon). The purchase price for the Sale Shares was arrived at on a willing-buyer willing-seller basis, and taking into account the pro rated amount (being 30%) of NTA of Songcheon of $1.74m. Sin Heng resumes trading at 1.00 p.m.

M Devt